The smartest LPs you’ve never heard of trimmed their China exposure in late 2024. They didn’t tell anyone.

By Q2 2025, three Singapore family offices we work with had quietly re-weighted around 18% of their Asia VC allocation toward what we call the Singapore-India corridor. By the time the rest of the market caught the story — sometime around the 2025 Super Return Asia panel circuit — the early movers were already up double digits, and the rest of you were still being told the 2022 playbook still worked.

It doesn’t.

If your Asia VC allocation is still running on the thesis you locked in three years ago, you’re not being conservative. You’re being mispriced. This piece is the practical map of what the corridor actually is, where the capital is now flowing, the three allocation shifts the smart money has already made, and the four sectors that will decide whether your 2030 returns look like 6× or like 1.4×.

It’s not for founders. It’s for the allocators rethinking their next commit.

Why the old Asia VC playbook broke in 2026

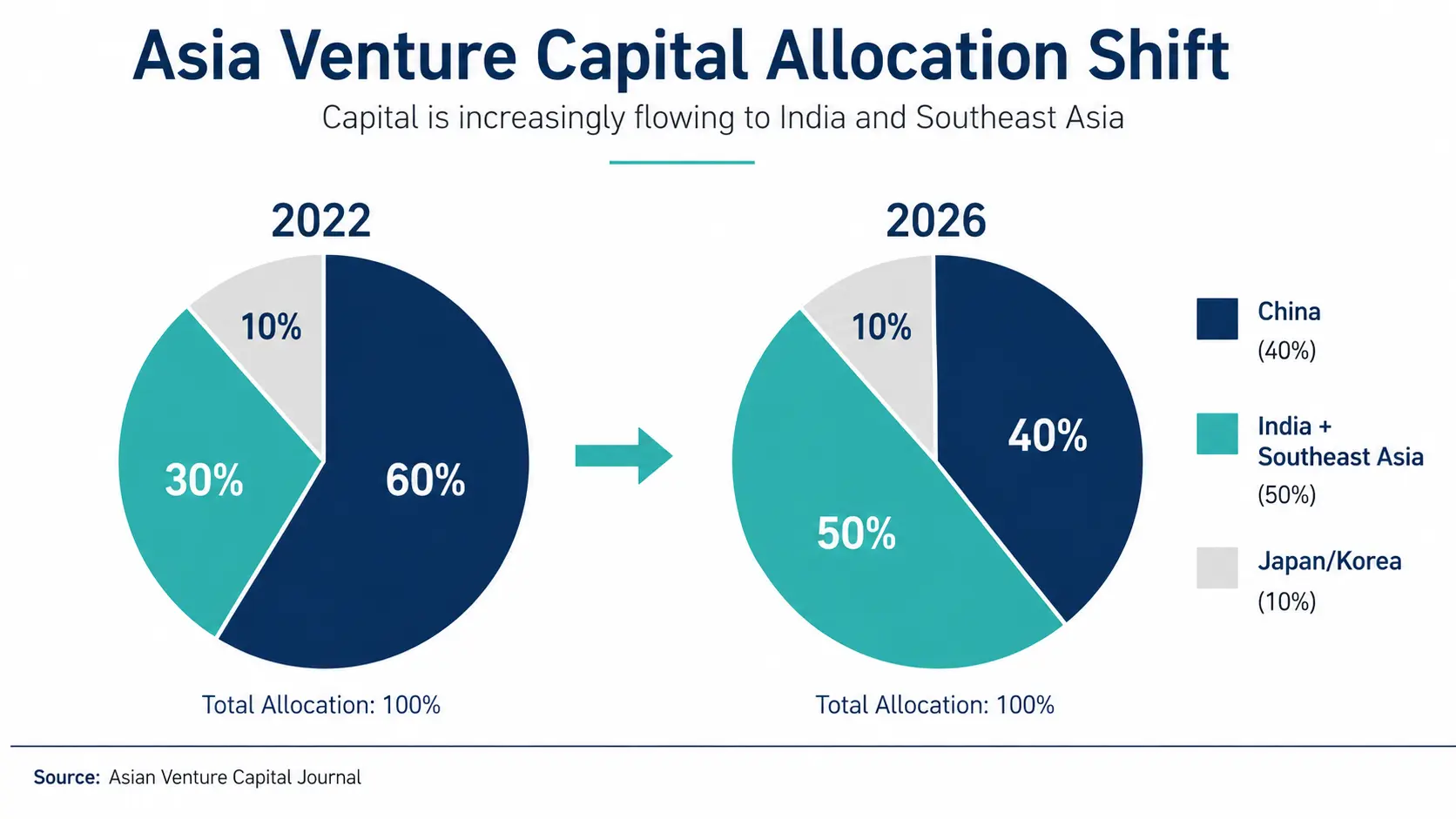

The 2022 Asia VC thesis was, broadly, a 60/30/10 allocation: 60% China, 30% India + SEA, 10% Japan/Korea. It assumed three things: that Chinese tech IPO windows would re-open, that India’s rupee depreciation was a temporary input, and that Southeast Asia’s startup ecosystem would mature on roughly the same timeline as India’s did between 2014 and 2019.

Each of those assumptions broke between 2023 and 2025.

The Chinese IPO window for VC-backed tech didn’t re-open in any meaningful way — Hong Kong listings recovered partially, US listings remained selectively closed for sensitive sectors, and the secondary market discount for China-exposed funds widened to levels that made marks look fictitious. Allocators who held to the 60% China weight saw IRRs compress, while their distributions stayed deferred.

India’s rupee story moved the other way. By late 2024, dollar funds investing into Indian startups were enjoying a tailwind from currency stability, the maturation of UPI as a distribution layer, and recent data showing record commitments to early-stage Indian VC funds.

Southeast Asia, meanwhile, finally got its secondaries market. Not because the public exits arrived — they mostly didn’t — but because the infrastructure for fund-of-funds and continuation vehicles caught up with the fact that 2018-vintage SEA funds were now in their distribution years. Liquidity unlocked. Allocators who believed they’d be locked into 12-year horizons discovered they could actually trade.

The corridor is what these three shifts produced together. Singapore as the legal-and-capital home, India as the talent-and-distribution engine. Neither alone matches what they do as a pair.

What the Singapore-India corridor actually is — and why the pair beats either alone

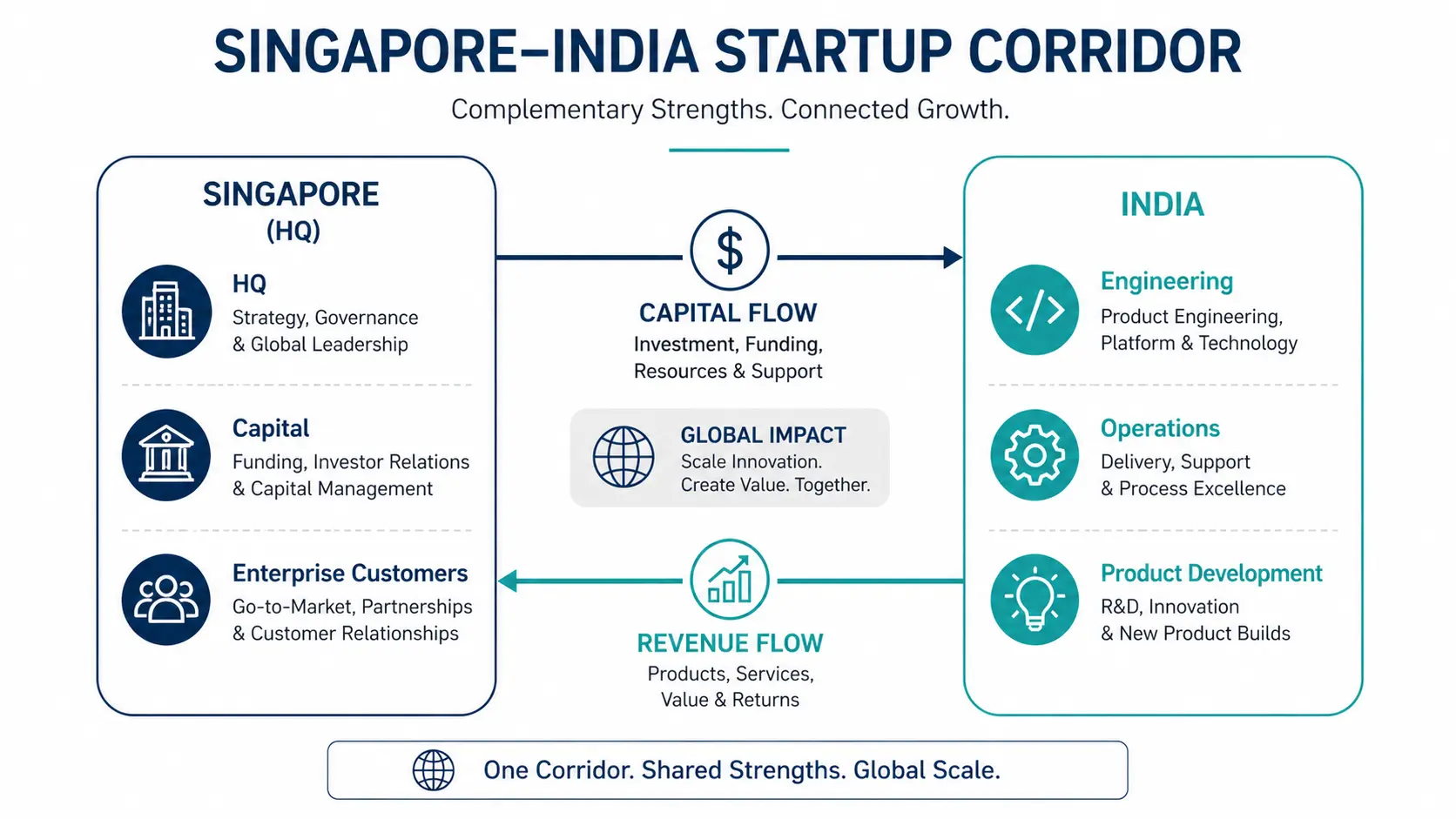

When we say “the corridor,” we don’t mean geography. We mean a stack.

A typical corridor company today incorporates in Singapore — often with a Variable Capital Company (VCC) structure for the holding entity — but builds its product and revenue engine in India. Engineering team in Bengaluru or Hyderabad. Sales motion split between Indian SMEs (volume) and Singapore-headquartered enterprise customers (margin). Capital raised in USD, deployed in INR, hedged where it matters.

This isn’t novel structurally. What’s new in 2026 is how fast the corridor compresses go-to-market timelines.

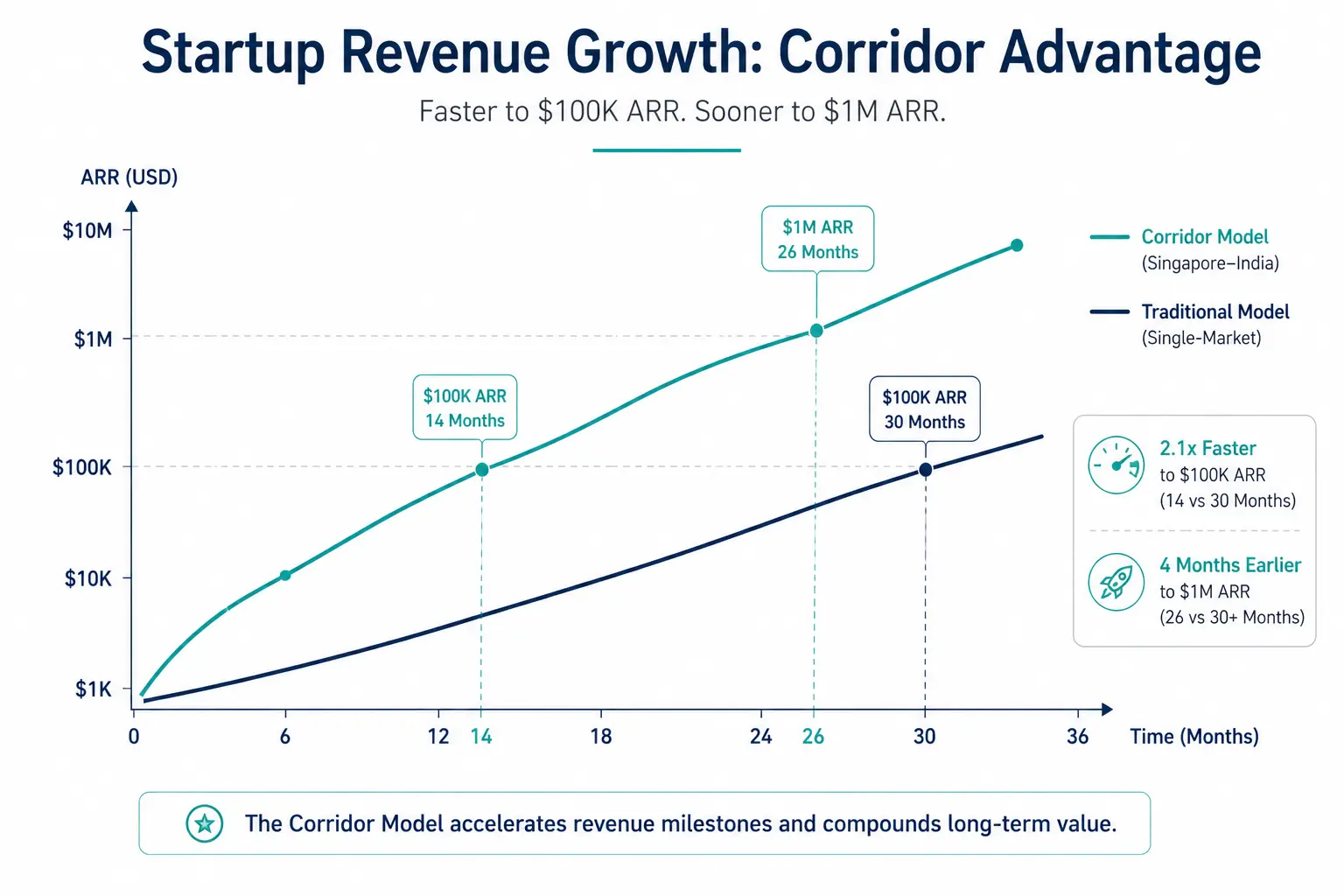

A pre-corridor SaaS company building for Asia might spend 18 months getting product-market fit in India, then another 12 months internationalising into Singapore-headquartered enterprise accounts. Total: 30 months to meaningful USD revenue.

A corridor-native company, in our portfolio data, runs both motions concurrently from month one. The Singapore HQ gives it banking, payment rails, and credibility to close enterprise pilots from day one. The India engineering base lets it ship fast enough that those pilots actually convert. Median time to first $100K USD ARR: 14 months. Median time to first $1M ARR: 26 months. (Anonymised, our portfolio Q1-Q4 2025.)

What this means for an allocator: the corridor is structurally faster on revenue compounding than either standalone India or standalone SEA. That’s the input. The output is shorter time-to-distribution at the fund level — and, when the fund is run by a manager who’s deliberately corridor-positioned rather than just opportunistically India-curious, lower DPI risk.

Standalone India funds are great. Standalone SEA funds are great.The pair, run as a single thesis, is structurally different. That’s why the dollar volume flowing into corridor-positioned funds in 2025 has grown meaningfully faster than standalone India and Southeast Asia funds, while standalone-India and standalone-SEA fund flows grew at a fraction of that pace.

Where the corridor money is actually moving — sector + stage breakdown

Stage-wise, the corridor is heavily weighted toward seed and Series A. Not because growth-stage capital has dried up — it hasn’t — but because the corridor structural advantage compounds most aggressively in the first 24 months of a company’s life. By Series B, the Singapore HQ premium is already priced in.

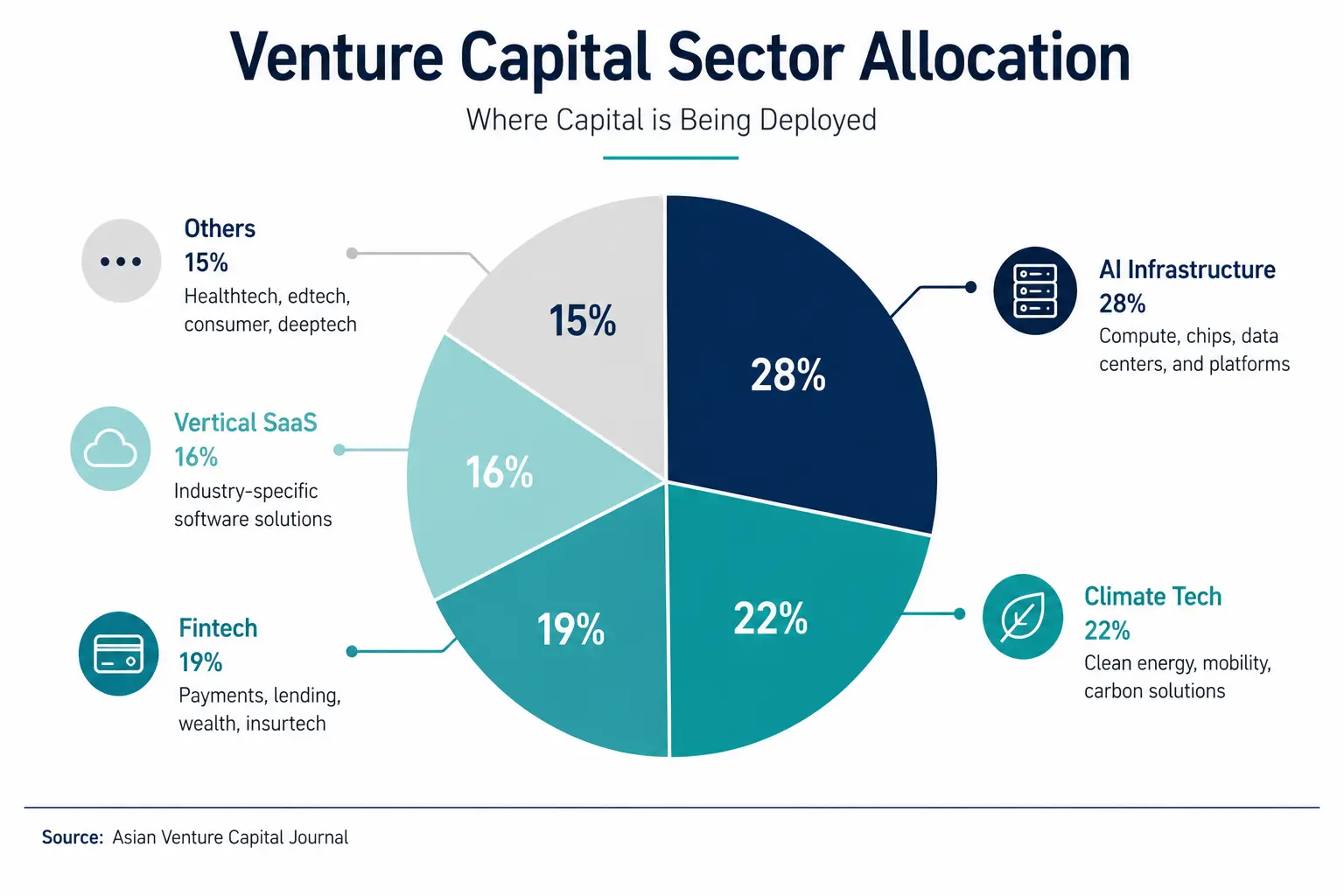

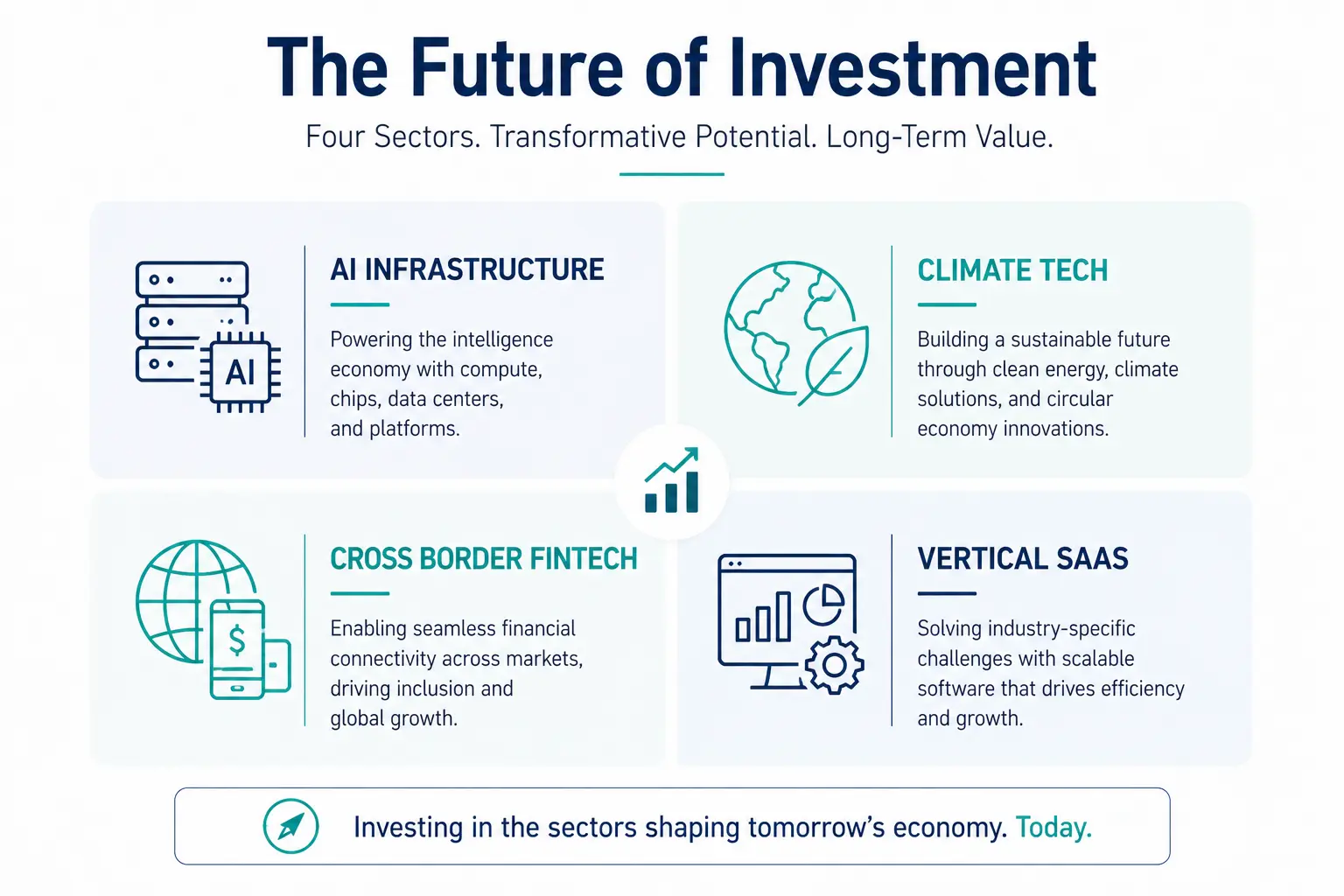

Sector-wise, the 2025 deployment data we track tells a clear story. Four sectors dominated:

AI infrastructure for emerging-market enterprise (28% of our tracked deployments). Not foundation models. The boring layer underneath — fine-tuning workflows, vector databases tuned for Indian-language data, RAG pipelines for compliance-heavy verticals like banking and insurance. India has the engineering depth; Singapore has the enterprise customers willing to pay USD.

Climate tech with credit-revenue dual models (22%). India’s rooftop solar, water-reuse infrastructure, and battery-recycling sectors got newly bankable in 2024 because of carbon-credit revenue streams that finally stabilised. Singapore-incorporated entities can sell those credits internationally; the India engineering layer builds the actual hardware.

Cross-border fintech for the Indian diaspora and SME export trade (19%). Not retail consumer fintech (saturated). Cross-border payments, trade finance, embedded finance for Indian SMEs exporting into SEA and the Middle East. UPI plus Singapore’s payment-rails maturity is a moat.

Vertical SaaS for Asia-specific industries (16%). Logistics for India’s port modernisation push, healthtech for Singapore’s aging demographic exported to India’s tier-2 hospital chains, agritech for Southeast Asia’s smallholder farmer financing.

The remaining 15% is a long tail of cybersecurity, deep-tech, and selective web3 plays — which we mostly avoid until the next cycle.

What’s striking is what’s NOT on this list. Consumer-facing apps. D2C brands. Pure-play crypto. Generative AI consumer products. Each of those was overweight in 2022 thesis allocations and dramatically underweight in corridor 2025 deployment. That’s not a coincidence. That’s allocators reading where the durable margin will live in Asia tech for the next decade.

The three allocation shifts the smart money has already made

Talking to the family offices and fund-of-funds we partner with, three quiet shifts happened in 2025 that haven’t been widely written about yet.

Shift 1: Shorter average hold on liquid public equities, more patient capital into private VC. Counterintuitive, because conventional wisdom says private allocation goes down when public markets get volatile. The 2025 data says the opposite. Family offices treated public-market volatility as the reason to redeploy out of liquid equities and into longer-duration private positions where mark-to-market noise doesn’t matter.

Shift 2: India weight up, China weight down — but not by reflex. The down-weight on China wasn’t ideological. It was DPI-driven. Funds with China-heavy portfolios were producing distributions at a quarter of the pace of India-weighted ones. Allocators followed the cash, not the geopolitical narrative. India’s distribution profile got better; China’s didn’t.

Shift 3: Climate tech moved from ESG line item to actual return line item. In 2022, climate allocations sat in a “do-good” bucket alongside impact investing — measured separately, returns-tolerated rather than returns-expected. In 2025, climate-corridor positions started competing with traditional VC on pure returns. Family offices we work with are now under-weighting traditional ESG funds and over-weighting corridor-positioned climate VC because the IRR profile finally pencils.

The allocators making these shifts aren’t the loudest LPs in the market. They’re the quietest. And they’re already two years into the trade by the time public commentary catches up.

If you’re reading this and thinking “we haven’t done any of these three” — that’s the asymmetric opportunity, not a problem.

4 sectors that will define corridor returns through 2027

Looking forward 18-24 months, here’s where we expect outsized corridor returns to concentrate.

Sector 1 — AI infrastructure for non-English enterprise data. Indian-language NLP, voice interfaces for Bharat-tier-2 markets, compliance-grade AI for Asian regulatory regimes. The English-first foundation models leave a moat-shaped hole here.

Sector 2 — Climate hardware with carbon-credit revenue layered on top. Battery recycling, water-reuse, distributed solar. The credit revenue makes unit economics work where they previously didn’t. Singapore-incorporated entities are the natural home for credit issuance, India does the build.

Sector 3 — Cross-border SME finance. UPI + India’s RuPay infrastructure + Singapore’s MAS-licensed payment rails = a real B2B moat for the SME exporter market. India has 6.3 million SMEs; a fraction of them export. The picks-and-shovels infrastructure for that fraction is dramatically under-built.

Sector 4 — Vertical SaaS for India’s tier-2 industries. Logistics, healthcare, agritech, education-services-for-overseas-jobs. Each vertical has a specific Asia-flavour that prevents Western SaaS incumbents from eating it. Hyderabad alone produced two corridor-positioned vertical SaaS companies in 2025 that are now at $5M+ ARR with US enterprise customers.

What corridor allocators will avoid (and this matters more than what they back): consumer crypto, generative-AI-as-product without infra moat, pure-play D2C, and any “global SaaS playing into India” thesis that doesn’t have an India-engineering, Singapore-HQ structure baked in.

The discipline of saying no is what separates corridor 2026 returns from corridor 2026 losses.

How Evolve Venture Capital is positioned for these shifts

Evolve Venture Capital was built corridor-first from day one. Not retrofit, not opportunistic — corridor as the founding thesis.

What that means structurally:

- Singapore HQ for the fund, with VCC compatibility for sophisticated LPs

- Mentorship-led portfolio construction — every founder gets named-partner sponsorship, not just check-and-board-seat coverage

- Active LP engagement: co-invest rights on every meaningful round, founder intros, quarterly portfolio deep-dives

- Singapore + India dual presence — partners on both sides, in-market rather than fly-in

Practically, that lets us see corridor-native founders six to nine months earlier than standalone-India or standalone-SEA funds, because we’re already in the room when a Bengaluru engineering team starts asking about Singapore incorporation. We’re not picking from a pre-formed pipeline; we’re shaping the pipeline at formation.

For an allocator evaluating a corridor commit, the questions to ask any GP are:

- Is your corridor position structural or opportunistic?

- What percentage of your portfolio is corridor-native at incorporation versus retrofit?

- How active is your LP engagement layer — in writing, with rights documented?

Evolve answers all three the way an LP would want them answered. Many of our peers don’t.

If your Asia VC allocation needs a corridor-positioned line, the conversation starts at evolvevcap.com/start-investing.

Frequently Asked Questions

Q: What is the minimum commitment to invest with Evolve VC?

A: Evolve VC is open to accredited investors and family offices. Minimum commitments vary by fund vehicle and investor profile; we discuss specifics in the qualification call. Start with a conversation: evolvevcap.com/start-investing.

Q: Is Evolve VC focused on Singapore startups or Indian startups?

A: Both — but as a single thesis, not as two separate buckets. We invest in corridor-native companies: Singapore-incorporated entities with Indian engineering and revenue motion. Standalone-India or standalone-Singapore deals are not our focus.

Q: What stage does Evolve VC invest at?

A: Primarily seed and Series A. The corridor structural advantage compounds most aggressively in the first 24 months of a company’s life. We selectively follow on into Series B for portfolio winners.

Q: How does Evolve VC differ from a standalone-India VC firm?

A: Standalone-India funds are excellent for deep-India deployment but typically lack the Singapore HQ pipeline structuring layer. Corridor-positioned funds — Evolve included — see deals at the corridor formation stage rather than at the Series A formation stage. That timing advantage compounds into return delta over a fund cycle.

Q: What return profile does Evolve VC target?

A: We target 4-6× net DPI over a 10-year fund cycle, with a TVPI target of 6-8×. These are targets, not guarantees, and reflect our corridor-positioning thesis described above.

Q: How can an LP evaluate whether a corridor commit fits their portfolio?

A: Three questions matter: (1) Is your existing Asia exposure structurally corridor-positioned or accidentally so? (2) What’s the DPI profile of your current Asia line? (3) Where in your fee budget does an additional Asia commit fit? We work through these in the qualification call.

The 2026 corridor opportunity is being priced right now, by allocators who started this trade in 2024. If your Asia VC line needs a corridor-positioned commit, start the conversation at evolvevcap.com/start-investing.