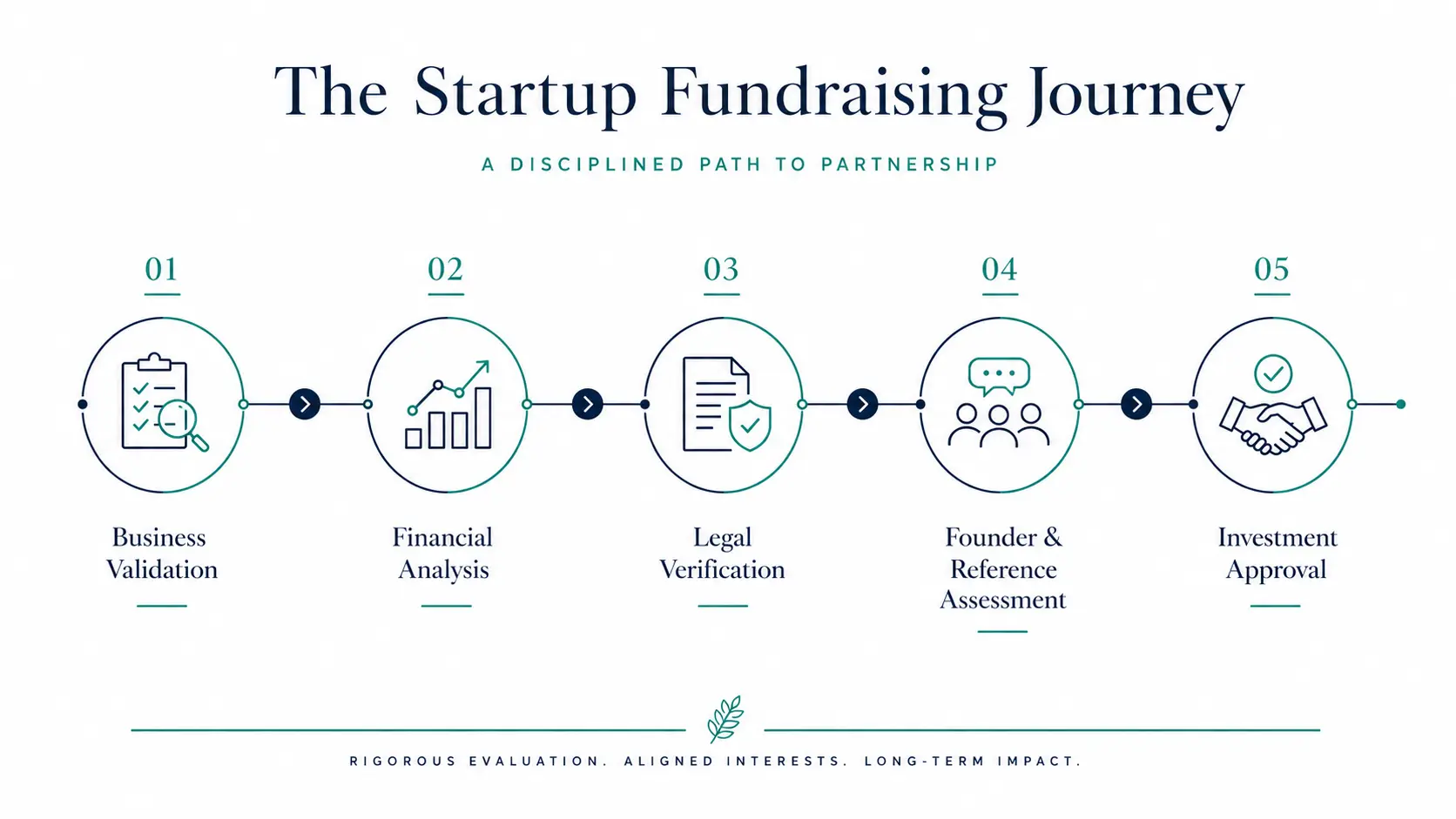

Getting to a term sheet is hard. Getting through due diligence is where most deals die — not because founders can’t answer the questions, but because they didn’t know the questions were coming.

This isn’t a problem of competence. Most Southeast Asian founders who lose deals in diligence are capable people building real businesses. The problem is information asymmetry. Investors run due diligence processes every month. Most founders go through one, maybe two, in their entire careers. The investor knows every trap in the room. The founder is walking in blind.

This guide closes that gap. What follows is a plain-language breakdown of exactly what institutional investors in Southeast Asia check during due diligence, in roughly the sequence they check it, and what you need to have ready before any of it starts.

The Due Diligence Timeline — What Actually Happens After You Get a Term Sheet

The term sheet is not the finish line. It’s the starting gun for the most intensive scrutiny your business will face until you go public.

Most founders assume due diligence is a document exchange — you send files, they review them, they wire the money. The reality is more layered. A standard Series A diligence process at a Southeast Asian institutional fund typically runs four to eight weeks and involves parallel workstreams that are happening simultaneously, often without the founder being aware of all of them.

Here’s the rough sequence:

Week 1–2: Business fundamentals review. The investor’s analyst team is building their own financial model from your numbers. They’re calculating metrics you may not have calculated yourself. They’re stress-testing your assumptions. This happens largely behind closed doors — you may not hear from the investor much during this period, which founders often misread as a bad sign. It usually isn’t.

Week 2–4: Legal and corporate structure review. The investor’s lawyers are pulling your incorporation documents, cap table, IP assignments, employment agreements, and any existing contracts with customers, vendors, or advisors. This is where undisclosed complications surface. If there’s a shareholder dispute from two years ago, a vesting schedule that wasn’t properly documented, or a contractor who built core IP without signing an assignment agreement — it comes up here.

Week 3–5: Reference checks. Investors are talking to people you didn’t introduce them to. Former employees, customers who churned, investors from your previous round, people who know you from before this company. This track runs quietly in the background while the legal and financial work is happening.

Weeks 4 to 6: Financial model audit and deal structuring. When the business and legal analysis is almost done, the investor goes back to the financial model, incorporating changes due to their analysis and starts dealing with the deal structuring.

Understanding this sequence matters because your job as a founder is different at each stage. In weeks one and two, you need clean financials that can be replicated by someone else. In weeks two through four, you need legal infrastructure that doesn’t surprise anyone. In weeks three through five, you need a reputation that survives conversations you’re not in.

Business Fundamentals Every Investor Calculates Before Your First Meeting

By the time a serious Series A investor in Southeast Asia sits down with you for a first meeting, their analyst has already built a preliminary model from whatever public information exists about your company — LinkedIn headcount, press releases, industry benchmarks. They know roughly what your burn rate should be. They have a range for what your ARR might be. They’ve estimated your CAC from your marketing spend.

This means the first substantive conversation is not about introducing your numbers. It’s about whether your numbers match what they already expect — and where they don’t, explaining why.

The specific metrics that get the deepest scrutiny:

Revenue quality. Not just ARR — the composition of ARR. What percentage is multi-year contracted? What’s the split between monthly and annual commitments? Are there any customers representing more than 15–20% of total revenue (customer concentration risk)? Has any revenue been recognized that isn’t yet collected?

Net Revenue Retention. This is the number that gets recalculated most often during diligence because founders frequently compute it differently from how investors do. NRR is expansion revenue plus contraction and churn, divided by starting period revenue, for the same cohort. If your best customers are growing but your average customers are flat or churning, your NRR tells a different story than your gross ARR growth.

Burn multiple. Net burn divided by net new ARR — how much capital are you consuming to generate each dollar of new recurring revenue? A burn multiple above 2 at Series A creates questions. Above 3 is a significant concern in the current environment.

Unit economics by customer segment. Not blended — by segment. Investors want to see whether your economics are good across the board or whether they’re carried by a subset of customers that aren’t representative of where you’re going.

Churn by cohort. Monthly churn numbers can hide structural problems. A startup with 2% monthly churn looks tolerable until you see that all of the churn is concentrated in the 6–12 month customer cohort, which means the product is not delivering value past the honeymoon period.

Team and Legal — The Surprises That Kill Deals Late

The deals that die in the final week of diligence almost always die because of a legal or team-related issue that surfaced unexpectedly. These are the areas where founders most consistently underestimate the level of scrutiny.

Cap table cleanliness. Every investor who has ever had a deal complicated by a messy cap table will spend disproportionate time checking yours. The specific things they’re looking for: is the cap table fully diluted and accurate? Are all vesting schedules properly documented and being tracked? Are there any uncapped convertible notes that could create unexpected dilution? Are there any shareholders whose contact information no one has, or who haven’t been heard from in years? Are there any side agreements with early investors or advisors that aren’t reflected in the standard shareholder agreements?

For Southeast Asian founders: the NVCA publishes model legal documents that represent global institutional standards for startup legal infrastructure. Familiarising yourself with these — available at https://nvca.org/resources/model-legal-documents/ — will help you understand what an investor’s lawyers expect to see and where your documents may diverge.

Did every founder assign their IP to the company at incorporation?

Did every contractor, especially early ones working for equity or below-market rates, sign an IP assignment agreement?

Is there any code in the product that was written while a founder was employed elsewhere — and if so, is there documentation that the previous employer has no claim?

Jurisdiction and structure. Many Southeast Asian startups have complicated holding structures — a Singapore holding company over an Indonesian or Vietnamese operating entity, or a Cayman Islands structure set up in anticipation of a US fund investment. Investors will examine whether these structures are properly maintained, whether transfer pricing between entities is documented, and whether there are any outstanding requirements from previous regulatory filings. If you have a Singapore-incorporated entity, the Monetary Authority of Singapore’s resources at https://www.mas.gov.sg/ are the relevant regulatory reference.

Employment agreements. Every employee should have a signed contract that includes a non-compete, a non-solicitation clause, and an IP assignment. Investors will check this. They’re specifically looking for: key employees who don’t have updated contracts, senior hires whose equity grants weren’t properly papered, and any promises made to employees that aren’t reflected in formal documentation.

The Financial Model Audit — What VCs Are Actually Looking For

Investors don’t review your financial model to see if it looks impressive. They review it to understand how you think — specifically, whether you understand your business at a level of detail that will make you a good steward of their capital.

The questions the model audit is designed to answer:

Do your assumptions have historical basis? Every growth assumption in a financial model should be grounded in something that has actually happened. A model that assumes 40% month-over-month growth because “the market is large” is not a financial model — it’s optimism with a spreadsheet wrapper. A model that assumes 15% month-over-month growth because that’s what happened in the last 6 months of focused outbound sales is a basis for a real conversation.

Does your headcount plan make sense? Investors will check whether your forecast headcount is consistent with your revenue projections. A model that shows revenue tripling with headcount growing 20% triggers questions about whether the model accounts for the operational complexity of scaling.

What are your gross margin drivers? Investors will decompose your gross margin assumptions by cost category and assess whether they’re realistic at scale. COGS that look attractive now because a founder is doing customer success work personally will look very different when that work is done by a 10-person CS team.

What happens in the downside case? Many founders present only a base case and an upside case. Investors always build their own downside case. If your model has no downside scenario, you’ll be asked to build one in the room — and how you respond to that request tells the investor as much as the numbers do.

For founders building their models: Carta publishes an annual State of Private Markets report with current benchmarks for growth rates, burn multiples, and unit economics across funding stages. It’s the most useful benchmarking resource available to founders for free.

The Reference Check — The Part Nobody Prepares For

The reference check is the part of due diligence that founders consistently underprepare for, because it’s the part they can’t directly control. But there is preparation you can do and founders who do it are in a fundamentally better position.

Investors typically run two types of reference checks. The first is formal — you provide a list of references, and the investor calls them. These are usually customers, co-investors, and advisors. Most founders handle this well because they control who goes on the list.

The second type is informal, and it’s where the real intelligence is gathered. Investors call people in their networks who know you, who worked with you, who were early employees, who left the company. They ask the same core questions: Is this founder someone you’d work with again? Were they honest when things were hard? Did they treat people fairly? Did they do what they said they’d do?

What this means practically: your reputation in the startup community — how you’ve treated every early employee, every advisor, every investor who passed, every co-founder — is your reference check. You can’t prepare for it the week before your term sheet. You can only behave consistently over the years that precede it.

What you can do proactively: reach out to former employees and early customers before you go into a raise. Understand where relationships stand. If there’s a founder dispute that ended badly, or an early employee who left unhappy, understand what that narrative might look like when an investor hears it.

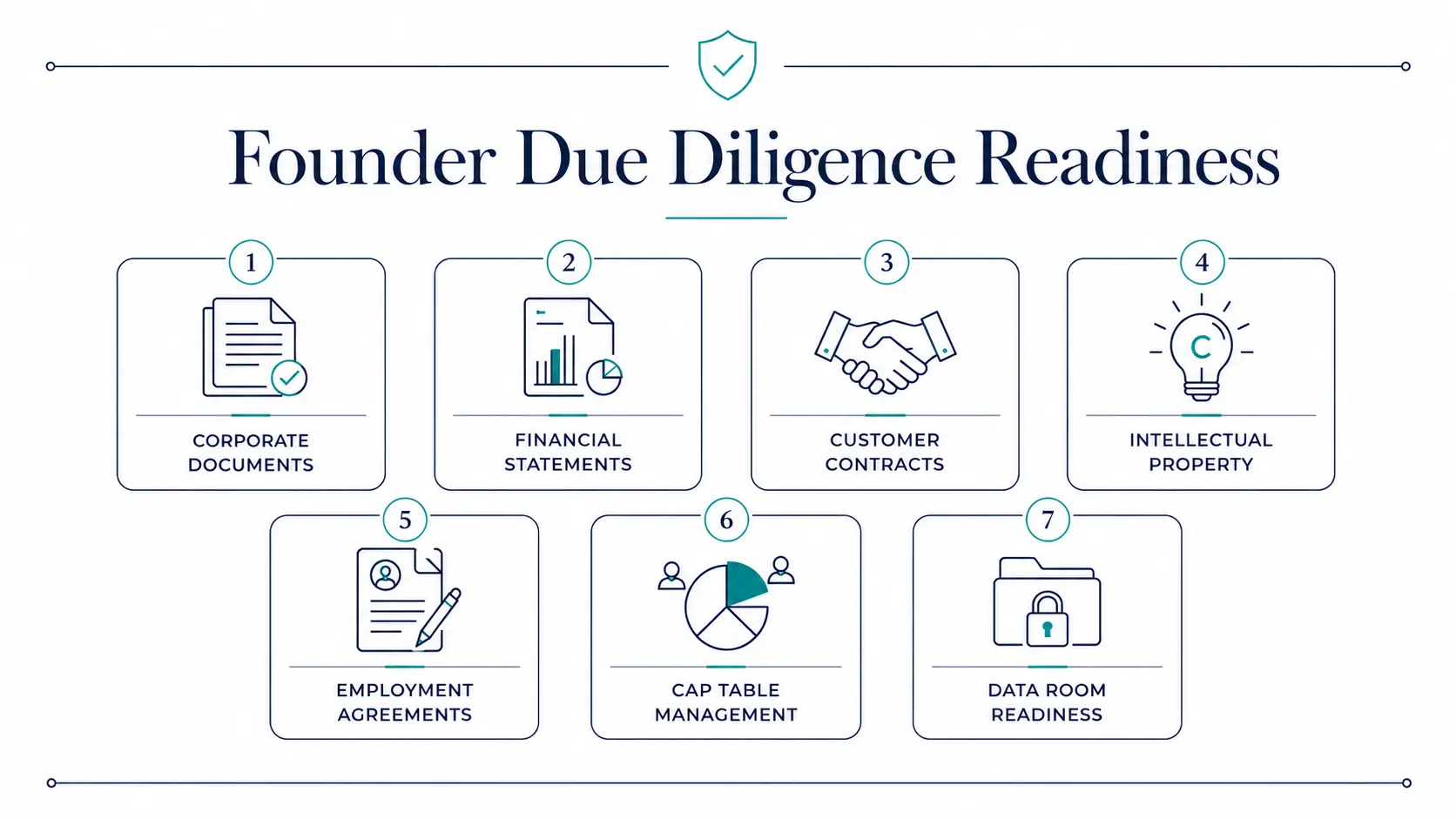

How to Prepare Your Data Room in 2 Weeks

A well-prepared data room doesn’t guarantee a deal. A poorly prepared one — or one that’s assembled reactively, file by file, as investors ask for things — significantly slows the process and signals operational disorganization that investors notice.

Here’s the core data room structure that meets institutional expectations for a Southeast Asian Series A:

Corporate documents: Certificate of incorporation, current articles of association/memorandum, all board resolutions, shareholder agreements, cap table (fully diluted, as of current date), all previous investment agreements (SAFEs, convertible notes, prior share purchase agreements).

Financial documents: 24 months of management accounts (P&L, balance sheet, cash flow), current month management accounts, 3-year financial forecast with assumptions documented, bank statements for the last 6 months, any outstanding loans or debt instruments.

Commercial documents: All customer contracts (or a summary of standard terms with exceptions noted), top 10 customer revenue breakdown, pipeline summary with stage and expected close dates, churn log with reasons.

Legal and IP documents: All IP assignments signed by founders and key contractors, trademark and patent registrations, any pending litigation or disputes, employment contracts for all current employees, standard NDA and contractor agreement templates.

Team documents: Org chart, option pool summary with individual grants, any advisor agreements with equity components.

The ILPA publishes standardized due diligence questionnaire templates at https://ilpa.org/ilpa-principles-3-0/ that represent what institutional-grade investors expect. While these are LP-focused, they give founders a clear sense of the documentation standards that institutional capital operates by.

Frequently Asked Questions

How long does VC due diligence typically take for a Series A in Southeast Asia?

For institutional Series A investors in Southeast Asia, a standard diligence process runs four to eight weeks from term sheet to close, assuming no material complications surface. Complexity in corporate structure, legal issues requiring remediation, or slow document provision by the founding team are the most common reasons processes extend beyond eight weeks. Founders who have a complete data room ready before the term sheet can sometimes compress the timeline to three to four weeks.

What’s the most common reason deals die in due diligence?

Legal and cap table issues cause more late-stage deal failures than financial underperformance. Specifically: undisclosed shareholder disputes, IP ownership gaps (code written by contractors without proper assignment agreements), and corporate structure complications from prior restructurings. Financial issues that were disclosed upfront rarely kill deals — undisclosed issues discovered in diligence almost always do.

Do investors check references with people I don’t provide?

Yes — and this is standard practice, not an anomaly. Investors will use their networks to find former employees, co-founders, customers, and peers who know the founding team. The best preparation is not to control the reference list — it’s to have behaved consistently and fairly throughout your company’s history so that these conversations support rather than complicate your raise.

Should I hire a lawyer before starting due diligence?

Yes, specifically a lawyer who has experience with venture capital transactions in the jurisdiction where your holding company is incorporated. The cost of legal support during diligence is significantly lower than the cost of a deal dying because a legal issue wasn’t handled correctly.

What happens if something surfaces in diligence that I didn’t disclose?

Disclosure and discovery are treated very differently by investors. Something disclosed upfront — a founder dispute, a past lawsuit, an IP complication — can usually be addressed and worked around if the rest of the business is strong. The same issue discovered during diligence, after the founder had the opportunity to disclose it, is almost always a deal-killer.

Due diligence is the part of fundraising that no pitch deck prepares you for. The investors who are deciding whether to wire you money are, at this stage, not evaluating your vision they’re auditing your execution. The founders who survive diligence intact are the ones who built clean legal infrastructure, know their numbers at a level of detail that can withstand scrutiny, and have a reputation that holds up in conversations they’re not part of.

None of this preparation happens in two weeks. It happens over the entire life of the company, in every decision about how to structure equity, how to handle difficult employee situations, and how to maintain financial records.

At Evolve Venture Capital, we work with founders across Southeast Asia at every stage of the investment process — including the diligence phase. Explore our investment philosophy or get in touch if you’re preparing for a raise and want a candid conversation about what to expect.