Most fund managers spend 80% of their time thinking about deals — sourcing, diligence, term sheets, portfolio support. LPs spend 80% of their evaluation time thinking about the fund manager. Not the portfolio. Not the thesis slide. The person and the team writing the checks.

That mismatch is at the center of why some funds raise their next vehicle with relative ease, while others — often with comparable returns — struggle. The good news: relationship management is a skill, not a personality trait, and it’s one most GPs have never been taught.

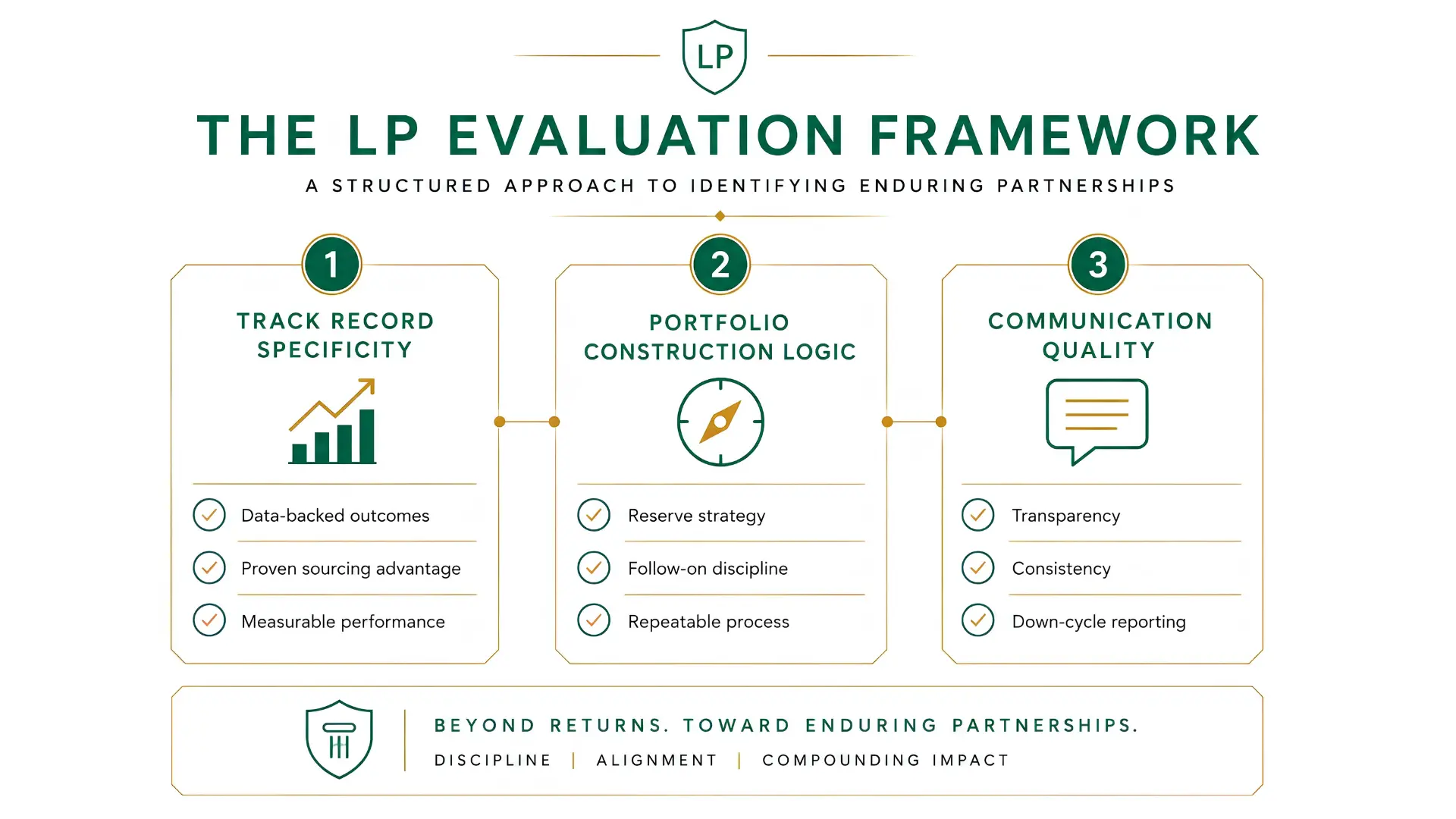

The LP Evaluation Framework Most VCs Don't Know Exists

Institutional LPs don’t evaluate a fund the way a founder pitches an investor. They’re running a structured assessment, even when it doesn’t feel like one in the room, and three dimensions tend to dominate.

GP track record specificity vs. category claims. “We have a strong track record in Southeast Asia” tells an LP almost nothing. “Across our last two funds, we led or co-led 60% of our Series A investments, and three of our top five performers came from founder relationships we’d built 12+ months before they raised” tells them everything. LPs are trained to discount category-level claims and weight specific, falsifiable detail. GPs who only have the former are, often without realizing it, signaling that they haven’t done the internal work of understanding their own edge.

Portfolio construction logic vs. a portfolio of bets. LPs want to understand the system that produced the portfolio — check size discipline, reserve strategy, follow-on decision criteria, sector and stage concentration limits. A portfolio that reads as “a collection of good companies we liked” versus “the output of a repeatable process” sends very different signals about whether performance is repeatable in Fund III, IV, or V.

Communication quality through down cycles. This is the dimension most GPs underweight — and the one LPs weight most heavily, because it’s the only one they can observe in real time, before returns are even knowable. How a GP communicates when a portfolio company is struggling, when markdowns happen, when the macro environment turns — that behavior is the single best predictor LPs have of how a GP will behave with their capital during the next downturn.

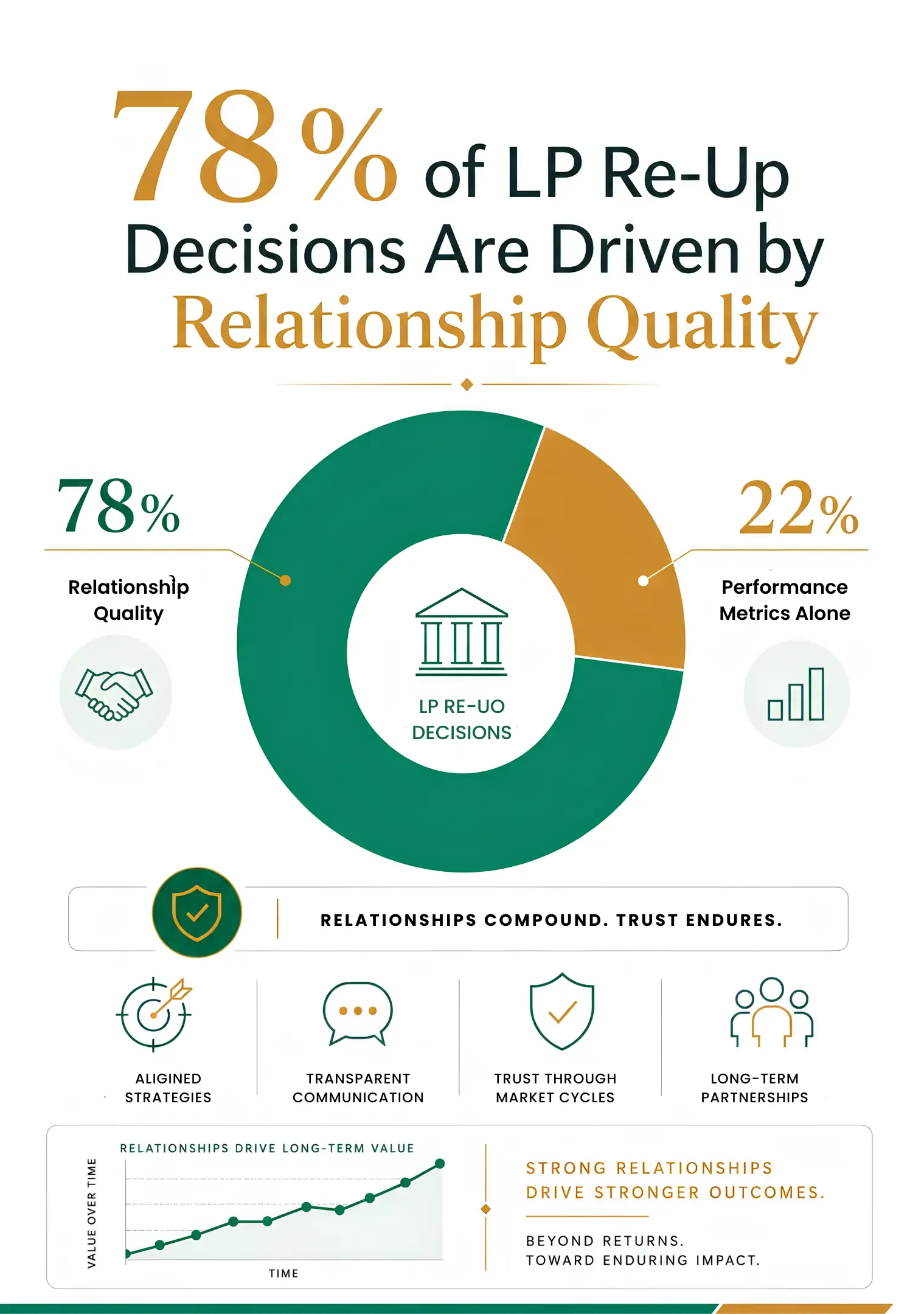

The 78% Statistic That Should Change How You Run Your Fund

According to Preqin’s 2026 LP Survey, approximately 78% of LP re-up decisions in Asia are driven primarily by relationship quality with the GP — not by fund performance metrics alone. This number tends to surprise GPs the first time they hear it, because it seems to contradict the idea that venture is a returns-driven business.

According to Preqin’s 2026 LP Survey, approximately 78% of LP re-up decisions in Asia are driven primarily by relationship quality with the GP — not by fund performance metrics alone. This number tends to surprise GPs the first time they hear it, because it seems to contradict the idea that venture is a returns-driven business.

It doesn’t contradict it. It explains how LPs actually assess returns. Performance numbers in venture are lagging, noisy, and — especially in early-stage funds — largely unrealized for years. An LP cannot fully evaluate a Fund II’s performance until well into Fund III’s life. What they can evaluate, continuously, is whether the GP communicates clearly, honestly, and consistently about what’s happening inside the portfolio.

What “relationship quality” actually means to institutional LPs. It is not warmth, charm, or how enjoyable annual meetings are — though those don’t hurt. It is, specifically: Does this GP tell me what I need to know, when I need to know it, in a way I can act on? Do they flag problems before I read about them elsewhere? Do their updates help me do my job — reporting to my own investment committee — or create more work for me?

The difference between quarterly reports and quarterly conversations. A quarterly report is a document. A quarterly conversation is a relationship touchpoint where an LP can ask follow-up questions, get color on a markdown, and — critically — observe how the GP handles being asked a hard question live. Funds that rely solely on the document, without the conversation, are leaving the most relationship-building part of LP communication unused.

The 5 Communication Failures That Cost VCs Their LP Base

These five patterns show up repeatedly in LP feedback on underperforming GP relationships — and every one of them is fixable without changing a single investment decision.

1. Over-reporting wins, under-reporting challenges. A portfolio update that’s 90% “here’s our latest unicorn markup” and silent on the three companies that are struggling doesn’t read as optimism to an LP — it reads as either denial or selective disclosure. Both erode trust faster than the bad news itself would.

2. Inconsistent update cadence. LPs build their own internal reporting cycles around when they expect to hear from GPs. A fund that sends detailed updates quarterly for a year, then goes silent for two quarters during a hard stretch, confirms the worst assumption an LP can make: that communication frequency correlates with how good the news is.

3. Generic investor updates not tailored to LP type. A family office LP, a fund-of-funds LP, and a sovereign-wealth-aligned LP are evaluating the same update through different lenses — liquidity timelines, co-investment interest, reporting requirements to their own stakeholders. A single generic update that ignores these differences misses the chance to make each LP relationship feel individually managed.

4. Missing the emotional intelligence layer. Numbers without context leave LPs to construct their own narrative — which is often more negative than reality. A markdown explained with “here’s what happened, here’s what we’re doing, here’s why we still believe in the team” lands completely differently than the same markdown presented as a bare number in a spreadsheet.

5. Treating LPs as capital sources rather than partners. LPs increasingly expect to be looped into portfolio company introductions, co-investment opportunities, and even informal market intelligence — not because they need the favor, but because it signals the relationship runs in both directions. GPs who only reach out when raising the next fund make that extractive dynamic obvious.

What High-Retention Fund Managers Do Differently

The GPs with the highest LP re-up rates share a small number of practices — none of which require additional headcount or a bigger budget.

Proactive bad news communication. The standard is simple: an LP should never learn about a significant portfolio company problem from anyone other than the GP, and never after the fact. Funds that consistently hit this standard report that LPs become more confident in them after a well-handled bad-news cycle, not less.

Segmented LP updates by interest area. Rather than one monolithic quarterly letter, high-retention GPs tag content by what different LP segments care about — liquidity-focused LPs get exit pipeline visibility, strategic LPs get co-investment flags, and so on. The core update stays the same; the framing and emphasis shift.

Annual LP advisory board practices. Even funds without a formal LPAC requirement increasingly run an annual (or semi-annual) session with key LPs — not a pitch, a working session — where GPs share portfolio construction thinking and get real feedback. This single practice does more for long-term retention than almost any other single initiative.

The “show your work” principle in portfolio decisions. When a GP explains why they followed on into one company and passed on another — the reasoning, not just the outcome — LPs gain visibility into the decision-making system itself. That visibility is what gives them confidence the system will work in the next fund, independent of any single company’s outcome.

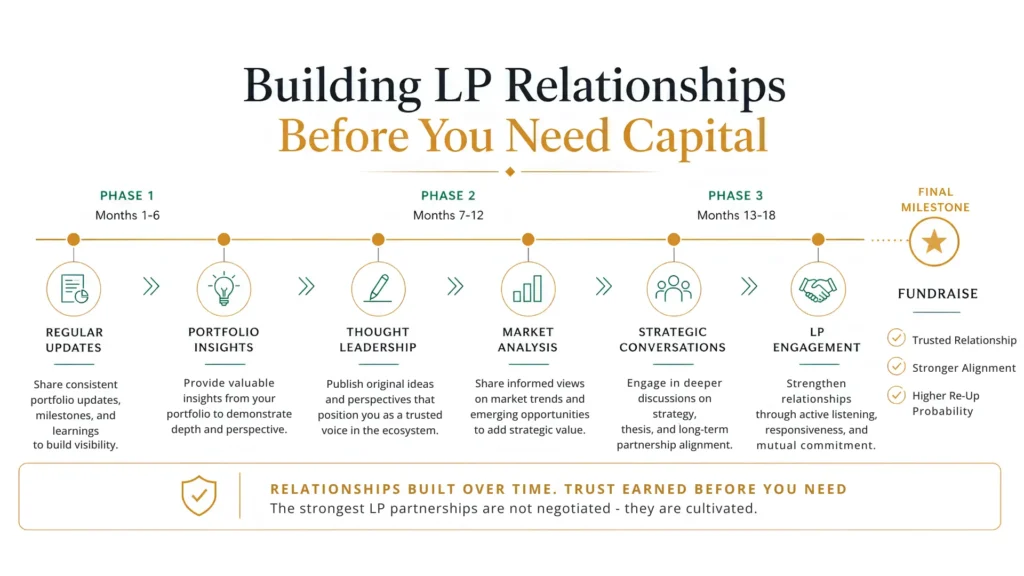

Building LP Relationships Before You Need Capital

The single most common mistake GPs make with LP relationships is timing: they invest in the relationship only during a fundraise, when the LP can feel — accurately — that the attention is transactional.

The 18-month relationship runway before a new fund raise. LPs who are approached cold, six months before a close, are evaluating a stranger. LPs who’ve been receiving thoughtful, consistent updates for 18+ months before that ask arrives are evaluating someone they already trust. The fundraise becomes a formality rather than a sales process.

Content strategy as LP relationship infrastructure. Public-facing content — market analysis, portfolio company spotlights, thesis updates — serves a dual function. It’s part of a fund’s broader market presence, but it’s also a low-friction way for current and prospective LPs to stay continuously informed about how a GP thinks, without requiring a scheduled call. Content becomes a relationship touchpoint that scales.

How EVC uses LinkedIn for LP touchpoints. At Evolve VC, our published market analysis — on shifts in Southeast Asian VC activity, sector theses, and portfolio company milestones — serves as an ongoing, low-pressure channel for LPs and prospective partners to see our thinking in real time, not just at fundraise checkpoints. It’s one part of how we approach our investment philosophy: relationships built over years, not quarters.

Frequently Asked Questions

Why do LP relationships matter more than fund performance for re-up decisions?

Venture fund performance is slow to materialize and difficult to fully assess until years into a fund’s life. Relationship quality — communication clarity, honesty during difficult periods, and responsiveness — is something LPs can observe continuously, making it the most actionable signal they have when deciding whether to commit to a GP’s next fund.

Which is the biggest problem GPs face while communicating with LPs?

Inconsistency in communication – communicating too much, and very enthusiastically, when things are going well, and shutting down at other times. It’s not a single act of negative information, but rather inconsistency that leads to loss of LPs’ trust.

How frequently should communication between GPs and LPs occur?

Apart from conventional quarterly updates, those GPs who maintain a high retention rate provide their investors with additional oral communication – phone calls or meetings that allow the LPs to raise questions on the spot. It is not important how often this happens; what is vital is its systematic nature and reliability.

How early should GPs start building relationships with prospective LPs for their next fund?

At least 12-18 months before an anticipated raise. LPs who have received consistent, substantive updates over that period are evaluating a known relationship rather than a cold pitch, which materially shortens and de-risks the fundraising process.

Returns matter — but in venture, they’re a lagging signal that LPs can’t fully evaluate in real time. Relationship quality is the signal they can evaluate, every quarter, in every interaction. The GPs who treat LP communication as core infrastructure — not an administrative afterthought — are the ones who find their next raise is a continuation of an existing relationship, not a new sales process.

To learn more about how Evolve VC approaches long-term partnership — with founders and with our capital partners — visit our About page and explore our investment philosophy.