The phrase “patient capital” gets used a lot in venture circles. Usually it’s positioning — a fund saying it won’t pressure founders to exit on a timeline that suits the fund life rather than the business. Most of the time it’s marketing copy. Sometimes it’s real.

The distinction matters more than most founders realise when they’re choosing investors, and the data behind it is more compelling than the conversation around it suggests.

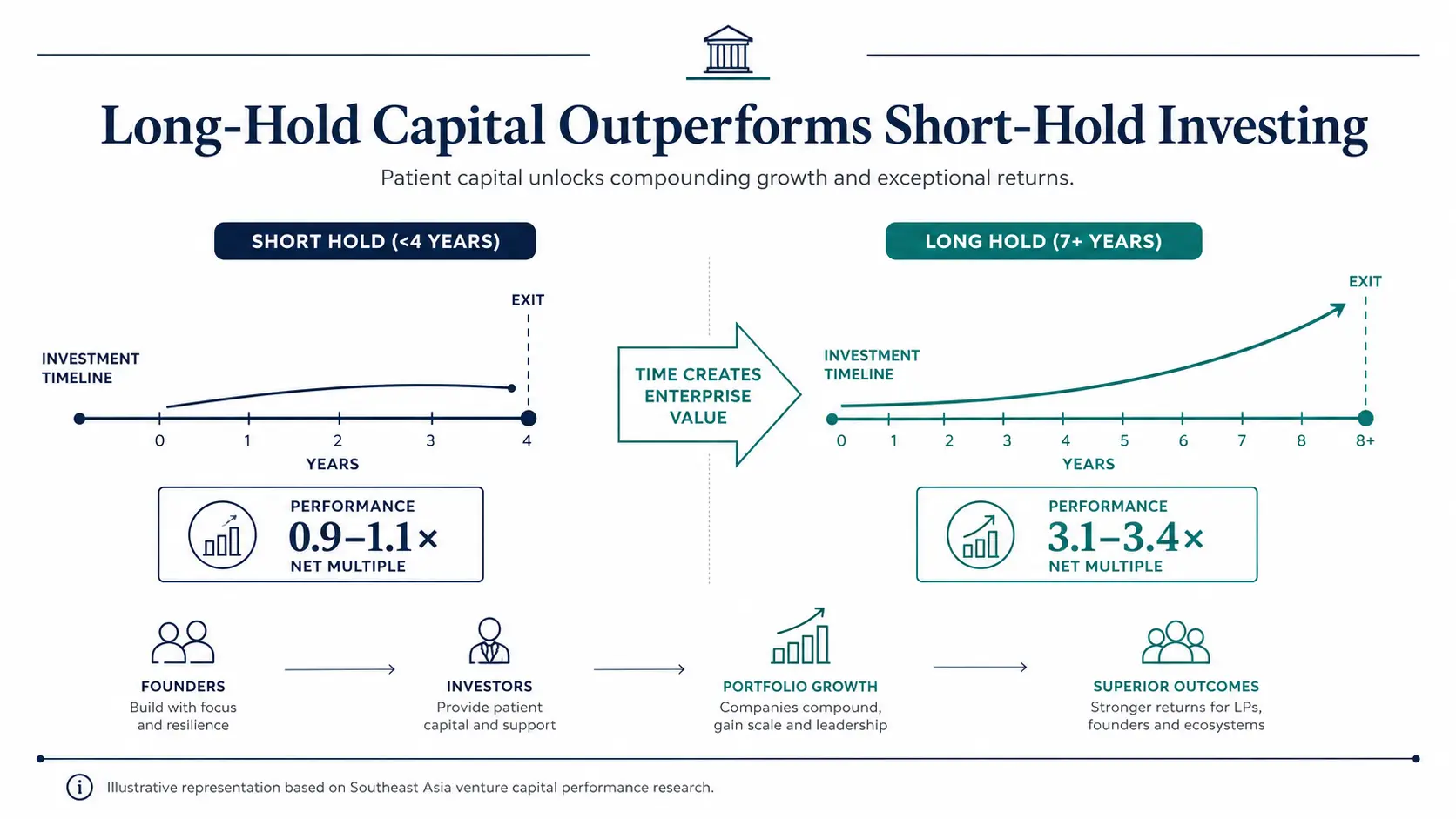

Here’s the core finding: Southeast Asian venture funds with average hold periods of 7 years or longer generate net multiples approximately 3.1–3.4x. Funds in the same region with average hold periods under 4 years average closer to 0.9–1.1x net to LPs. The gap isn’t driven by sector choice or deal sourcing quality — it’s driven almost entirely by whether the fund had enough time for its best companies to reach their actual potential.

That finding should change how founders think about which investor to take money from. It should also change how LPs think about the funds they back.

What the Return Data Actually Shows

The comparison between short-hold and long-hold VC performance in Southeast Asia isn’t a new debate, but the data has become clearer in the last two years as more funds have reached full realisation or near-realisation of their portfolios.

Cambridge Associates’ annual venture benchmark data — available at https://www.cambridgeassociates.com/research/ — shows consistently that the top-quartile performing venture funds globally maintain portfolio companies for a median of 7.2 years from first investment to exit. Bottom-quartile funds, by comparison, show median hold periods of 3.8 years. The return differential between top and bottom quartile is not subtle: top-quartile funds generate net IRRs roughly 2.5 to 3 times higher than bottom-quartile funds from the same vintage.

In Southeast Asia specifically, the dynamic is amplified because of two regional characteristics. First, the exit environment is less liquid than US or European markets — fewer IPO windows, fewer strategic acquirers operating at scale, and secondary markets still developing. A company that needs to exit in year four because the fund is approaching its deployment deadline is exiting into a thinner market and accepting worse terms. A company that can wait until year seven or eight exits when it’s genuinely ready and when market conditions support a fair valuation.

Second, the best businesses in Southeast Asia take longer to build. Regulatory navigation, multi-market expansion, and the process of educating customers in markets where the product category is still developing — these are not two-year projects. A B2B SaaS company targeting Indonesian SMEs needs 18 months just to understand the buying process well enough to build the right sales motion. A climate tech company working in Vietnam needs 24 months of relationship-building with government procurement before a significant B2G contract is realistic. The fund that arrived with a 4-year deployment timeline and a 5-year hold expectation was never going to capture the full value of these businesses. The one willing to run a 9-year vehicle is.

Why Founders Desperately Need Patient Partners — And Often Don't Realise It

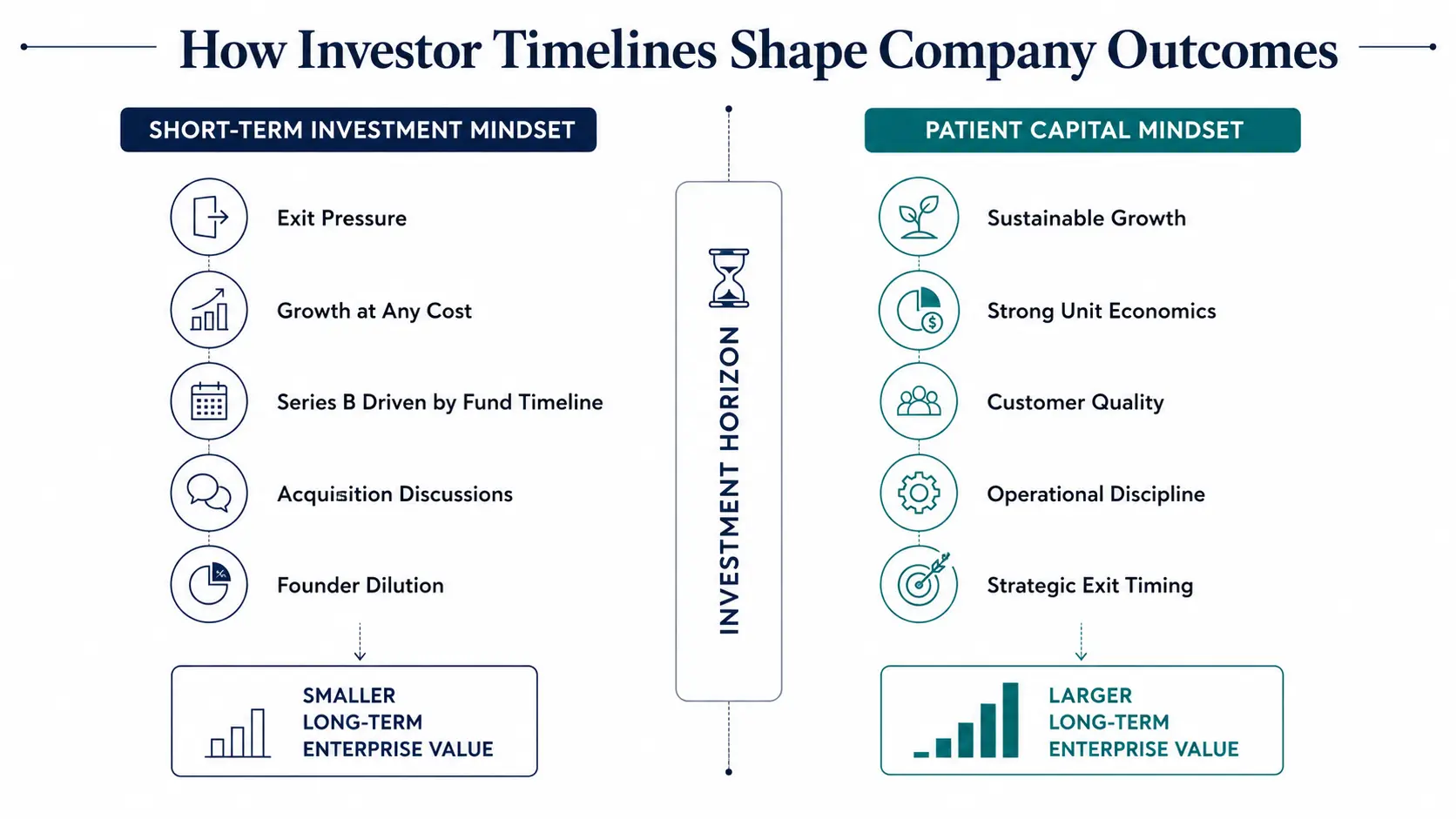

Most first-time founders evaluate investors on three things: brand, check size, and how much they liked the partner. The one thing that has the most direct impact on their long-term outcome — fund life and hold period expectations — rarely comes up in the conversation at all.

Here’s what actually happens when a founder takes capital from a fund with a short hold expectation that doesn’t align with their business timeline:

The artificial milestone problem. The fund needs to show the portfolio company making progress toward an exit every 12–18 months. This creates pressure for the kind of metrics that look good in a deck — user growth, GMV, headline ARR — even when the underlying business health metrics (retention, unit economics, operational leverage) aren’t ready to support an exit at a price anyone would be happy with. Founders end up optimising for the wrong outcomes.

The board dynamic shifts. As a fund approaches year 5 or 6 of a typical 10-year structure, the pressure to generate DPI (distributed capital) starts to dominate board conversations. Suddenly the investor who was a supportive partner in years 1–3 is the one asking every quarter whether the company has had any acquisition conversations. This shift is not personal — it’s structural. But it completely changes the nature of the investor-founder relationship.

The Series B trap. When a fund with a short hold expectation needs an exit but the company isn’t ready to be acquired, the fallback is to push for a Series B that brings in a new investor who might eventually buy the company out. The result is dilution the founder didn’t need at a time that wasn’t optimal, managed by an investor whose timeline agenda was driving the decision.

None of this happens with a fund that entered the investment with a realistic view of how long the business actually needs to reach its potential. The conversation never shifts from “how do we build the best company” to “how do we get to an exit.”

Two Paths, Same Company — An Anonymized Case Study

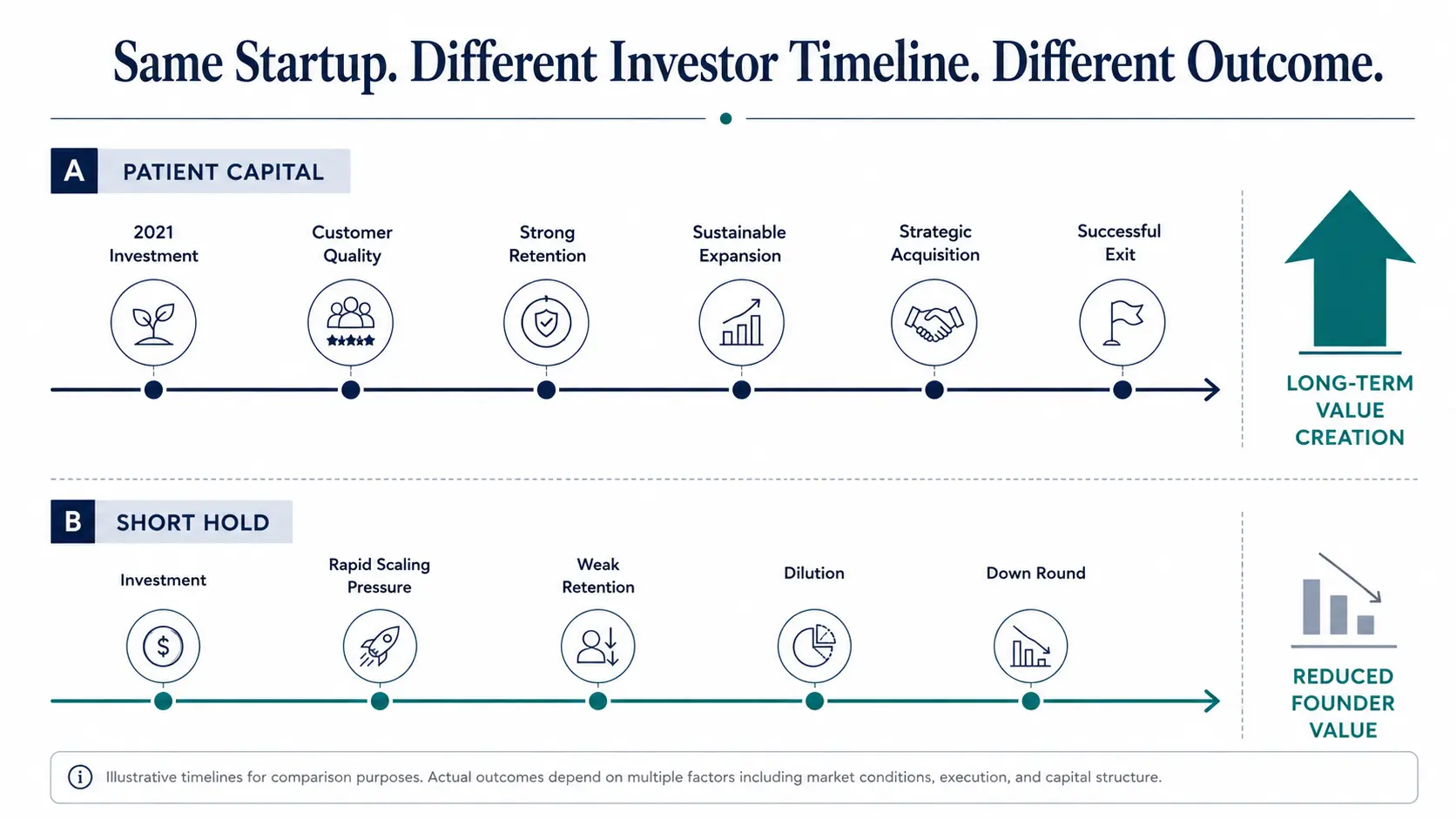

Consider two versions of the same B2B logistics technology company, Series A in Indonesia in 2021, $8M raised.

Version A: Fund with 8-year expected hold. The investor’s thesis was that Indonesian logistics infrastructure would take 5–6 years to reach the maturity where the software layer became truly valuable. The board was explicitly aligned that the company should prioritise unit economics and customer depth over headline growth. By 2025, the company had 140 enterprise customers, 94% net revenue retention, and a waiting list. In 2026, a strategic acquirer paid $180M. Founder and employee equity returned approximately 4.7x on the invested capital.

Version B: Fund with 4-year expected hold. Different investor, same vintage, similar deal terms. The fund needed to show portfolio progress by 2024 to support fundraising for their next vehicle. Board pressure pushed the company toward aggressive customer acquisition — GMV and user numbers that looked compelling but came at the expense of onboarding quality and retention. By 2024 the company had grown fast but had 71% NRR and a shrinking average contract size. No strategic acquirer was interested at a price above the preference stack. The fund marked the position down in 2025. Founder equity was essentially underwater.

The company, the market, and the team in both versions were identical. The investor timeline was not.

What Patient Capital Actually Requires From Founders

Patient capital is not a gift. It comes with its own expectations, and founders who receive it without understanding those expectations create friction with their investors in ways they didn’t anticipate.

Transparency over optimism. A fund with a 7–9 year hold has made a long commitment. They are not expecting a straight line to success — they are expecting honest communication about what’s actually happening, including the parts that are hard. Founders who manage their investor communications like a PR exercise, emphasising wins and minimising challenges, tend to erode the trust that makes long-hold relationships work. The value of patient capital is largely delivered through the quality of board support during difficult periods — and that support depends on the investor knowing what’s actually going on.

Operational discipline over growth at all costs. Patient capital doesn’t mean unlimited runway to figure things out. It means the investor is willing to let the business develop on its natural timeline — but that timeline needs to show compounding improvement in unit economics, customer quality, and operational capability. A business that is unprofitable at year 5 with no clear path to profitability is not being patient — it’s being undisciplined. Patient investors are watching for the former and very concerned about the latter.

A genuine long-term vision, not a positioning statement. Founders who pitch patient investors with a long-term vision but make every decision for the next quarter have a fundamental mismatch. Patient capital is most valuable for founders who genuinely have a 7–10 year view of the business they’re building — who can say clearly what they’re building toward and why short-term shortcuts would undermine it.

How to Identify Genuinely Patient Investors Before You Take Their Money

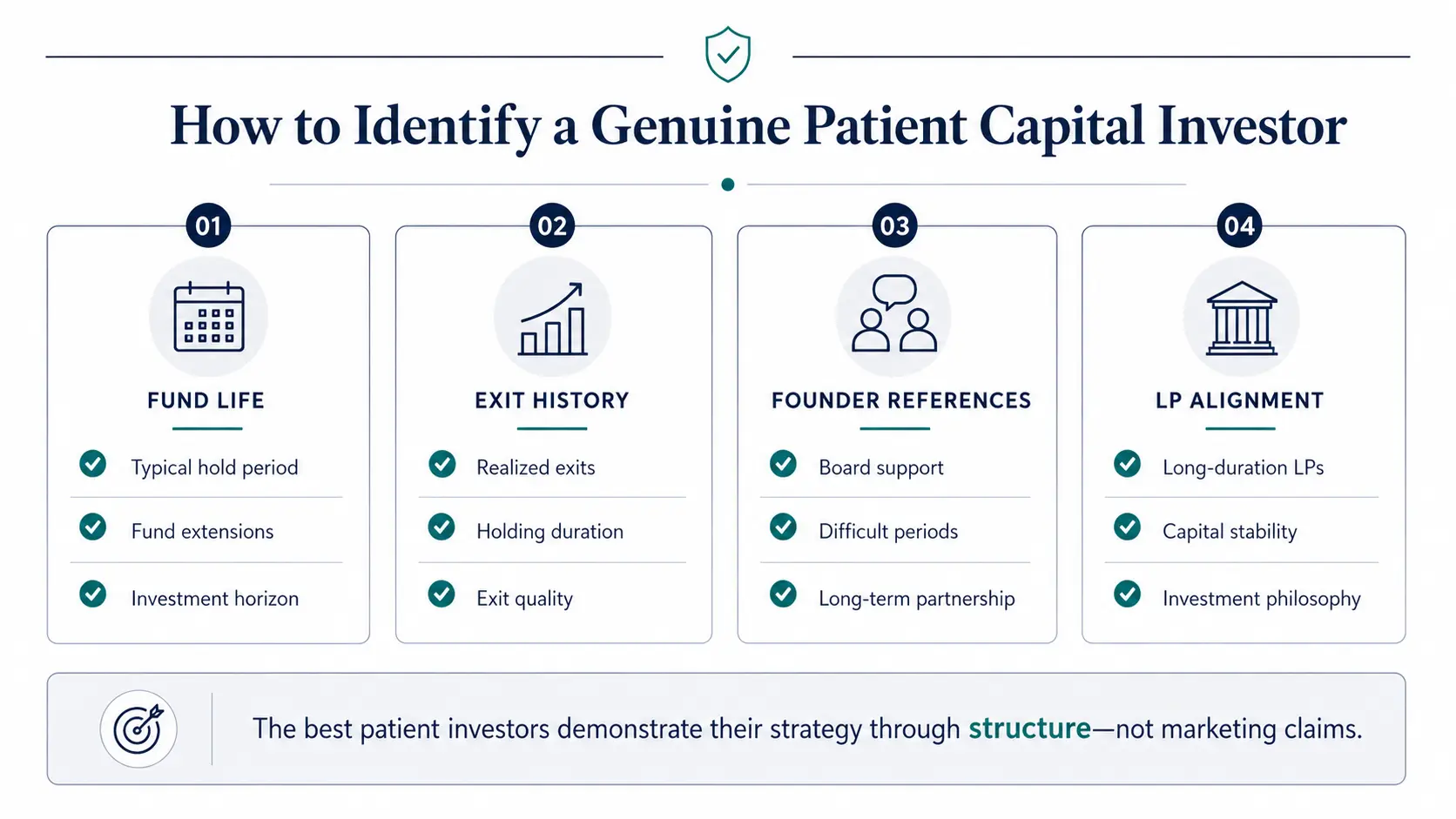

The most important thing to understand is that “patient capital” as a self-description is nearly universal among VCs and tells you nothing. Every fund says they’re long-term oriented. The evidence is in the structure and the track record, not the pitch.

Ask about fund life and extension history. A fund with a standard 10-year life and one extension option is not unusual. A fund that has consistently extended multiple vehicles tells you something about their underlying orientation toward hold period. Ask directly: “What is your typical hold period for your best-performing companies?” The answer should be specific, not a range of “it depends.”

Check their realized exits. Ask for examples of exits from prior funds — specifically, the hold period from first investment to exit for their top three outcomes. A fund that says they’re patient but where every top exit happened in years 3–4 is revealing its actual behavior regardless of what it says about philosophy.

Talk to portfolio founders. The single best data source on whether an investor is genuinely patient is founders who’ve experienced a difficult period with that investor. When the company was under pressure, what did the board conversations look like? Did the investor push for decisions that served the fund’s timeline or the company’s actual needs?

Look at their LP base. Funds with long-hold orientations tend to have LP bases that are structurally patient — endowments, long-duration family offices, development finance institutions. Funds that are primarily backed by fund-of-funds with their own liquidity pressures tend to reflect those pressures in their portfolio management behavior, regardless of what they tell founders. Preqin’s fund database at https://www.preqin.com/insights/ provides LP composition data for institutional funds that is worth reviewing for any fund you’re seriously considering.

Frequently Asked Questions

What is patient capital in venture capital?

Patient capital in venture capital refers to investment capital committed with a longer-than-standard hold period expectation — typically 7–10 years or more — rather than the traditional 5–6 year timeline. It reflects the investor’s willingness to let portfolio companies develop at their natural pace rather than forcing exits or milestones to suit the fund’s liquidity timeline. In Southeast Asia, where market maturation timelines are longer, patient capital is a structural advantage for both investors and founders.

Do patient capital funds generate lower returns because they hold longer?

No — the data consistently shows the opposite. Cambridge Associates’ benchmark research demonstrates that top-quartile performing funds (which generate significantly higher returns) also maintain longer average hold periods. The mechanism is straightforward: more time allows the best companies to reach their full potential value, and forces the investor to make decisions that serve the company rather than the fund’s liquidity schedule.

How do I know if an investor is genuinely patient or just using it as marketing language?

Ask for specific data: the average hold period across their prior fund’s realized exits, examples of companies they held for 7+ years, and the reasoning behind their longest holds. Also speak directly with founders from their portfolio who’ve been through difficult periods — how the investor behaved when things were hard is the most reliable indicator of their actual orientation.

What does patient capital expect from founders in return?

Primarily: transparency, operational discipline, and genuine alignment with a long-term vision. Patient investors are not passive — they expect honest and frequent communication, measurable improvement in business fundamentals over time, and founders who are building for the long game rather than optimising for short-term metrics. The relationship works best when both parties have explicitly aligned on what the business needs to look like in year 5 and year 8, not just year 2.

Is Evolve Venture Capital is a patient capital fund?

Evolve Venture Capital structures its investments with hold period expectations aligned to what the specific business and market require — typically 6–9 years for our climate tech and digital infrastructure investments in Southeast Asia. We believe the most durable outcomes in the region come from giving companies the time to build properly, and our LP base is selected to reflect that orientation.

The returns data is not ambiguous. In Southeast Asia, the venture funds generating the best outcomes for both LPs and founders are the ones that entered their investments with a realistic timeline and maintained it through the inevitable difficult periods. The ones that didn’t are the ones with the cautionary case studies that never get published.

For founders choosing investors, the timeline question should rank alongside valuation, board governance, and pro-rata rights as a non-negotiable point of diligence. The investor you want is the one who will still be your advocate in year six, when the business is genuinely valuable but not yet at its full potential — not the one who’s already started suggesting acquisition conversations because their fund needs DPI.

At Evolve Venture Capital, long-hold, patient investing is not a positioning choice — it’s how the math works for the kinds of companies we back in Southeast Asia. Learn more about how we invest, or get in touch if you’re building something that deserves more than a 5-year runway.