Cap table management doesn’t get discussed nearly enough in Southeast Asia’s founder community — until it starts killing rounds.

We’ve sat across the table from founders raising Series A and B who had done everything right in their business but had cap tables that made institutional investors uncomfortable. Not because the numbers were wrong. Because the structure was messy: too many early angels with no lead and no pro-rata clarity, convertible notes with aggressive valuation caps, ESOP pools that hadn’t been refreshed, or dual-class share arrangements with no sunset provisions.

In Singapore specifically, cap table conventions sit somewhere between US venture norms and the more relationship-driven structures common in India. Understanding where Singapore sits — and what the institutional venture capital firms in Singapore expect to see at each stage — is critical for any founder raising in the SEA corridor.

This is what we look at, what we’ve seen go wrong, and what a clean Singapore cap table should look like at every stage of growth.

What a Singapore Cap Table Actually Is — and Why It's Not Just a Spreadsheet

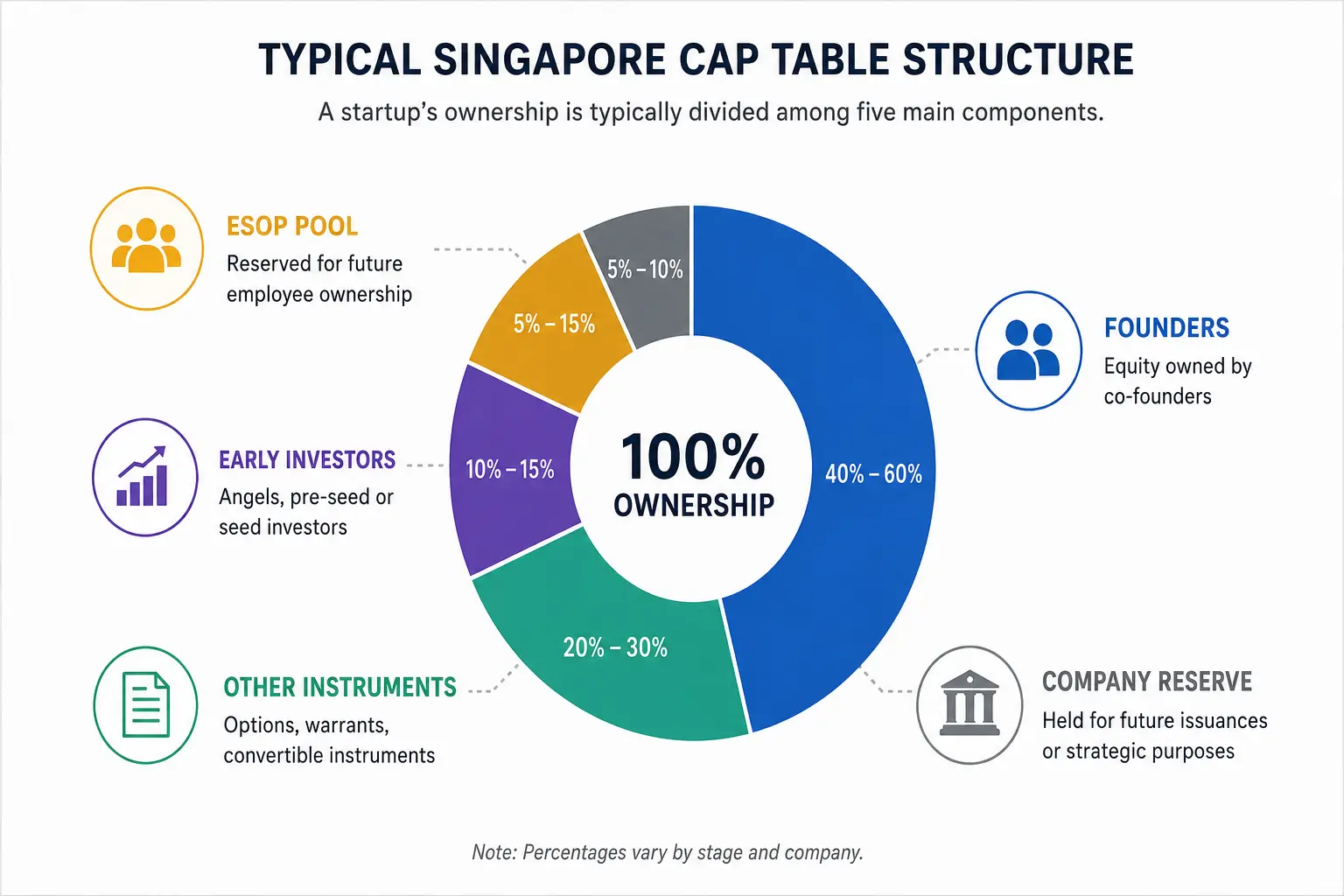

A capitalisation table — cap table — is a legal record of equity ownership in a company. In Singapore, it reflects ordinary shares, preference shares, convertible instruments (SAFEs, convertible notes), ESOPs, and any warrants issued.

At incorporation, a Singapore company is registered under the Companies Act with the Accounting and Corporate Regulatory Authority (ACRA). Share issuances, transfers, and shareholder agreements must align with the company’s constitution provisions and are legally binding records.

What most early-stage founders misunderstand is that a cap table is not merely a financial record — it is a governance document. It tells investors who has decision-making rights, who can block transactions, who has information rights, and who dilutes whom under what circumstances. A cap table with 15 individual angel investors, no lead, and no coordinated shareholder agreement is not just administratively messy — it is a genuine material risk to every future fundraising round.

Stage-by-Stage: What the Cap Table Should Look Like

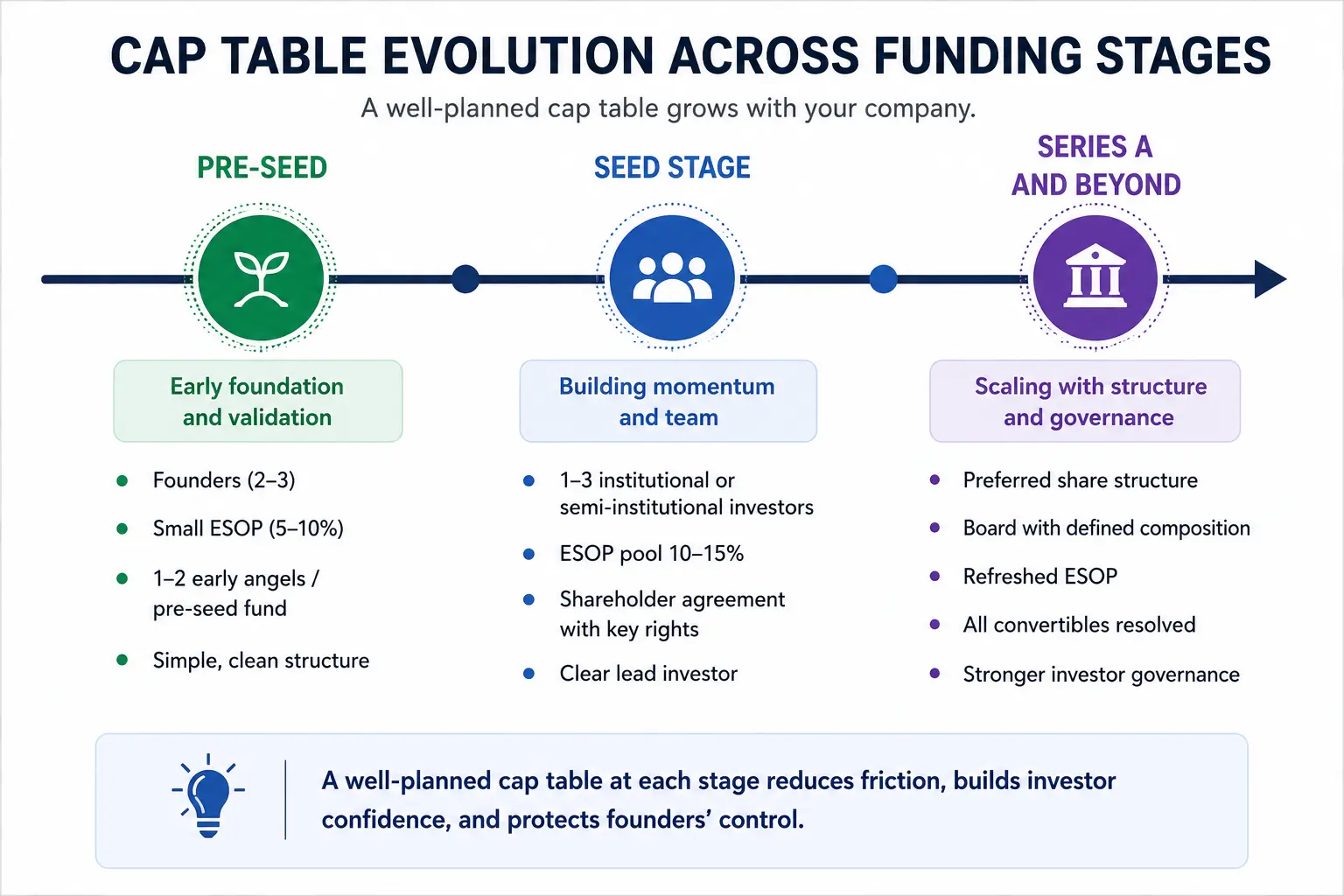

Pre-Seed

At pre-seed, a Singapore cap table is typically clean: founder shares (usually split between 2–3 co-founders), a small ESOP pool (5–10%), and one or two early angels or a pre-seed fund.

The most common error at this stage is founders issuing shares directly to early advisors, friends-and-family investors, or mentors without proper documentation — or at inconsistent valuations. By the time a seed or Series A investor reviews the cap table, they see fragmented ownership with no documentation trail. This raises questions about governance discipline that are difficult to answer convincingly under due diligence pressure.

Use a SAFE (Simple Agreement for Future Equity) for early informal investment wherever possible. It delays the valuation conversation to a point where founders have more negotiating leverage, and it keeps the formal cap table clean until a priced round is warranted.

Seed Stage

A well-structured Singapore seed round typically involves 1–3 institutional or semi-institutional investors — angel syndicates, family offices, or seed funds — an ESOP pool of 10–15%, and a shareholder agreement that clearly defines information rights, pro-rata rights, and reserved matters requiring investor approval.

At this stage, as an early-stage VC in Singapore, we look at the following:

Is there a lead investor, or is the round fragmented across 8–10 individuals with no coordination mechanism? Has the ESOP pool been sized to accommodate hiring through Series A without requiring a separate re-approval vote? Do any convertible instruments carry aggressive valuation caps that will create significant founder dilution at the next priced round? Is there a drag-along provision allowing a majority of shareholders to force a sale, or does one small early investor have effective blocking rights?

The cleanest seed rounds in Singapore are those where a credible lead has been established, documentation is NVCA-aligned or Singapore-adapted equivalent, and founders retain meaningful control through a clearly structured preference share or dual-class arrangement with fair governance provisions.

Series A and Beyond

By Series A, institutional investors — particularly those from the US or managing US LP capital — will want to see a clean preference share stack. In Singapore, this typically means: participating or non-participating preferred shares with a 1x liquidation preference, anti-dilution provisions using weighted average methodology (not full ratchet), board composition clearly documented (typically 2 founder seats, 1 lead investor seat, 1 independent at Series A), option pool refreshed before the round closes, and all prior convertible instruments converted or resolved.

The Monetary Authority of Singapore (MAS) framework and guidance published by the Singapore Venture and Private Capital Association (SVCA) provide useful benchmarks for best-practice term sheet structures for Singapore-incorporated entities. Founders entering Series A negotiations should be familiar with both before sitting down at the table.

The 5 Cap Table Mistakes That Kill Singapore Rounds

1. Too Many Angels with No Lead and No Pro-Rata Clarity

When a seed round has 12+ individual investors with small cheques, no lead, and no coordinated shareholder agreement, Series A investors face a structural coordination problem. Passing reserved matters resolutions, issuing new shares, or executing an acquisition requires majority consent — and reaching 14 individual angels across different time zones is operationally costly and genuinely risky.

More subtly, it signals that the founders were unable to attract a credible lead. That signal, however soft, registers with every investor who reviews the cap table. The fix: consolidate early angels into an SPV (Special Purpose Vehicle) wherever possible. One SPV means one cap table entry, one signature on shareholder resolutions, one coherent voice in investor communications.

2. Convertible Notes with Aggressive Valuation Caps

A convertible note with a $500K valuation cap converting at Series A when the company is priced at $6M creates enormous founder dilution and signals to incoming investors that the company took aggressive terms under funding pressure.

Y Combinator’s SAFE documentation recommends uncapped SAFEs with MFN (Most Favoured Nation) clauses for early-stage rounds where possible. This structure is increasingly adopted by sophisticated Singapore seed funds. If you have outstanding notes with aggressive caps, the time to renegotiate is before your next raise — not during it.

3. ESOP Pool That Is Too Small and Refreshed Too Late

Founders consistently underestimate ESOP requirements and refresh timing. By the time a Series A company needs to hire a CFO, VP Engineering, and Country Manager, the original pool is exhausted — and going back to shareholders for a re-approval vote mid-fundraise is disruptive and signals poor planning to prospective investors.

Standard guidance from most venture capital firms in Singapore is to establish a 15% ESOP pool at seed, sized to accommodate hiring through to Series A close. The pool should be formally approved at the same time as the seed round, as a single board resolution.

4. Full Ratchet Anti-Dilution

Full ratchet anti-dilution means that in a down round, early investors’ shares are repriced entirely to the new lower price — protecting their ownership percentage at the direct expense of founders and employees.

While this appears in some markets, it is viewed as aggressive within Singapore’s institutional VC community. Weighted average anti-dilution is the accepted norm for credible institutional investors in the region. Any term sheet presenting full ratchet should be pushed back on directly and early.

5. Dual-Class Shares with No Sunset Provision

Dual-class share structures are legally permissible in Singapore and increasingly common as a mechanism for preserving founder control. The problem arises when there is no sunset clause — a condition under which dual-class shares automatically convert to ordinary shares, typically tied to IPO, change of control, or a founder departing the business.

Without a sunset, institutional investors managing capital from US or European LPs may face governance concerns that prevent their participation. If you are implementing dual-class structures, build in clear, fair, and proportionate sunset provisions from day one — not as a negotiating concession later.

What We Look For When We Review a Cap Table

At Evolve, cap table review is a standard component of initial due diligence on every company we consider backing. Here is specifically what we assess:

Founder ownership and alignment. If the founding team collectively holds less than 40% by seed stage, that raises questions — not because the number is inherently disqualifying, but because it often reflects early dilution decisions made under duress or without proper counsel. Founders need meaningful equity to remain incentivised through a 7–10 year company-building journey.

Clean convertible instrument stack. All convertible instruments should be clearly documented with reasonable caps and an unambiguous conversion mechanism that creates no uncertainty at the next priced round.

Adequate ESOP pool. We want to see a pool sized for the next 18 months of hiring — not just today’s headcount. Under-sized ESOPs at seed create predictable problems at Series A, and we factor that into our assessment of execution risk.

Governance structure. Who are the shareholders? Are SPVs in place with clear governance provisions? Is a shareholders’ agreement properly executed and filed? Who holds information rights, and are those rights appropriately scoped?

No undisclosed commitments. Side letters, informal promises to future investors, verbal equity commitments — these surface eventually, always at the worst possible moment. We prefer to find them in diligence than after a term sheet has been signed.

Building a Cap Table That Attracts Capital Rather Than Repelling It

The cap table conversation is not a one-time event at incorporation. It is an ongoing governance discipline. Founders who treat it as such — reviewing their structure every six months and proactively cleaning up issues before they become due diligence blockers — consistently raise faster and on better terms than those who treat the cap table as an administrative afterthought.

The companies in Southeast Asia that successfully compound through multiple funding rounds share one structural characteristic: their founding teams understood early that a clean, well-documented cap table is a form of respect for future investors’ time. It signals governance awareness, access to credible legal and financial advice, and a company built to scale — not just survive the next 12 months.

If you’re raising in Singapore and want an honest assessment of your cap table structure before your next round, connect with us at Evolve. We will tell you exactly what we see — including the things you may not want to hear, and specifically how to address them before they become problems.