There’s a quiet reallocation happening in Southeast Asian venture capital right now, and most founders and fund watchers are missing it because they’re looking at the wrong data.

The headline number — seed funding in SEA down roughly 50% from its 2022 peak — tells one story. But inside that compressed total, one category is moving against the trend: climate tech. Not because investors have become idealists. Because the numbers are starting to work in ways they didn’t three years ago.

This piece is EVC’s analysis of where institutional capital is actually flowing in SEA climate tech in 2026, what’s driving it, and what fundable opportunities look like in the current environment.

The Capital Rotation No One Is Talking About

The 2024–2025 correction in Southeast Asian VC hit consumer tech, late-stage growth, and marketplace models hardest. These were the categories that attracted the most capital during the 2020–2022 expansion, and they’ve seen the sharpest pullback as investors recalibrated toward capital efficiency.

What didn’t pull back — and in some sub-sectors actively expanded — was climate-adjacent infrastructure. The reason is structural: climate tech in Southeast Asia is increasingly intersecting with government procurement, bilateral development finance, and corporate sustainability mandates that create revenue certainty investors in the consumer tech space simply can’t access.

A B2G (business-to-government) climate tech deal in Indonesia or Vietnam has a fundamentally different risk profile than a consumer subscription business in the same market. The contract sizes are larger, the relationships are stickier, and the regulatory tailwind — driven by net-zero commitments across ASEAN members — is creating demand that isn’t going away in a downturn.

This doesn’t mean all climate tech is fundable. It means the specific intersection of climate technology, institutional revenue streams, and defensible IP is where disciplined investors are concentrating attention while pulling back everywhere else.

The Blue Economy — $24 Trillion and Still 1% Funded

The ocean economy — marine energy, sustainable aquaculture, blue carbon, marine biotech — represents what the KPMG Ocean Capital Report 2026 estimates at $24 trillion in addressable economic value globally. The venture capital investment into this space, globally, remains under 1% of what the category’s scale would imply.

In Southeast Asia, that underinvestment is particularly stark — and the opportunity is particularly concentrated. The region contains some of the world’s most biodiverse and economically significant marine ecosystems: the Coral Triangle spanning Indonesia, Malaysia, and the Philippines; Vietnam’s 3,000-kilometer coastline; Thailand’s aquaculture economy; and Singapore’s emerging position as the hub for blue economy financial structuring.

Three specific sub-sectors within the blue economy are attracting disproportionate early institutional attention:

Sustainable aquaculture technology. Southeast Asia produces over 35% of the world’s farmed seafood. The technology stack — precision feeding, disease detection, water quality monitoring, logistics optimization — is still largely manual and fragmented. Startups applying IoT, sensor technology, and AI-assisted monitoring to existing aquaculture operations have clear, immediate customers and quantifiable ROI. This isn’t a “build the market” situation — the market is paying for this already, just from less sophisticated providers.

Blue carbon credit infrastructure. The voluntary carbon market has seen significant volatility, but one category of credits has held value through the turbulence: blue carbon — credits generated by protecting or restoring coastal ecosystems including seagrasses, mangroves, and salt marshes. Southeast Asia holds approximately 33% of the world’s mangrove coverage. The infrastructure to measure, verify, issue, and trade blue carbon credits is still being built. The companies building that infrastructure — measurement platforms, verification methodologies, credit issuance technology — are fundable in a way that many offset-category investments are not.

Ocean-based renewable energy logistics. Offshore wind is expanding rapidly across Vietnam, Taiwan, and the Philippines. The logistics, installation, and maintenance infrastructure for these assets is a massive, underserved market that requires deep regional knowledge to navigate. This is less “breakthrough technology” and more “critical infrastructure services” — which, from an investor’s perspective, is often more fundable than the headline innovation.

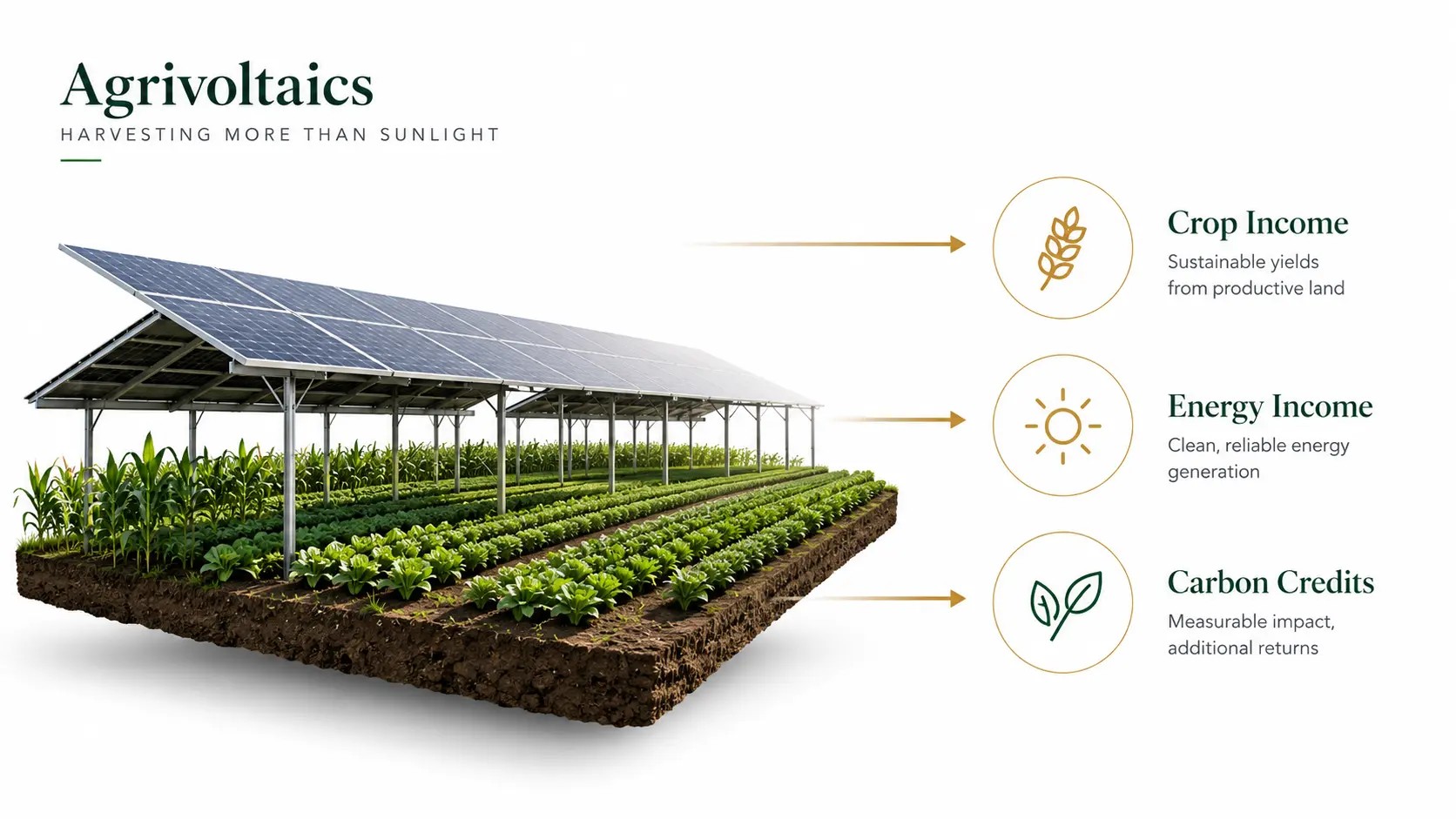

Agrivoltaics — Why Arid Land Is Becoming a Premium Asset

Agrivoltaics — the co-location of solar energy generation with agricultural activity on the same land — is one of the most underappreciated emerging categories in Southeast Asian climate tech. And it connects directly to one of the region’s most underutilized resources: dryland and semi-arid land that is currently either idle or marginally productive.

The basic model works like this: elevated solar panels are installed over agricultural land at a height that allows farming below. The shading effect from the panels reduces water evaporation in the soil, which improves crop yields in arid conditions. The panels themselves generate renewable energy for local consumption or grid sale. The combination — improved agricultural productivity plus energy revenue on previously marginal land — creates an economics story that neither agriculture nor solar alone could tell.

In the context of Southeast Asia, where Indonesia alone has approximately 14 million hectares of underutilized dryland, the potential scale is significant. Several pilots in Java and Sulawesi are showing dual-income outcomes that are commercially interesting at relatively modest capital deployment.

The fundable opportunity here is primarily in the technology and services layer — precision farming systems designed for agrivoltaic conditions, monitoring platforms, project development expertise, and carbon credit methodology development — rather than in owning the land itself.

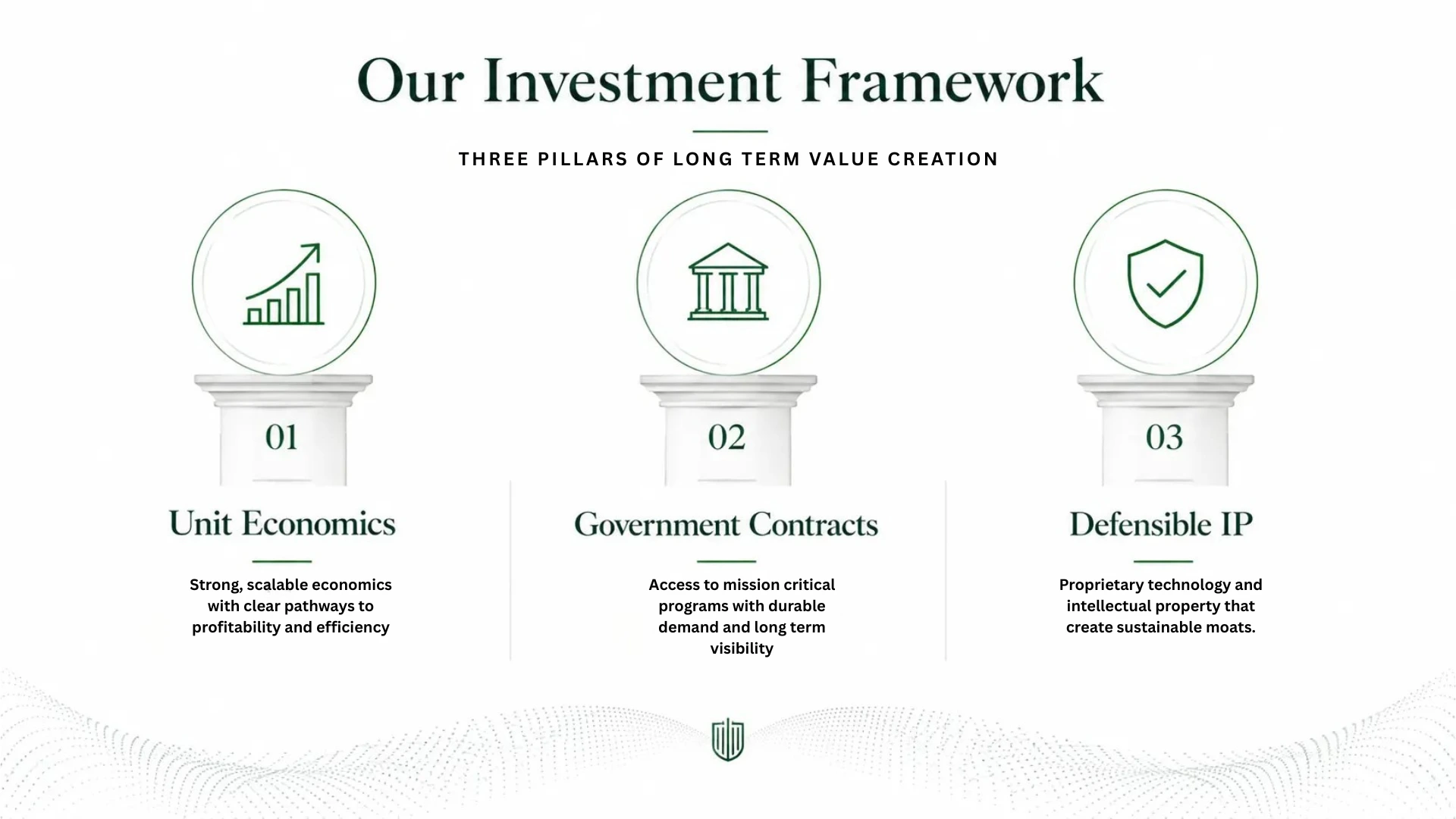

What Fundable Climate Tech Actually Looks Like in 2026

Not all climate tech is fundable, and the category’s genuine importance doesn’t make every pitch investable. Based on current deal flow in SEA, three characteristics consistently define the climate tech companies that are closing rounds:

Demonstrable unit economics that don’t depend on carbon credit prices. The companies raising money in 2026 have a primary revenue stream — equipment sales, service contracts, government procurement — and treat carbon credit revenue as upside, not as the core financial model. Climate tech that can show a compelling P&L without any carbon revenue, and then layer carbon revenue on top, is dramatically easier to fund.

B2G revenue anchors in the pipeline. The most fundable climate tech startups in SEA right now have at least one government or development-finance-institution contract in progress or closed. These contracts validate market need in a way that B2C or even B2B pilot deals can’t match.

IP that is genuinely proprietary. “We’ve built a platform” is not defensibility. Proprietary measurement methodology, hardware that performs materially better than commercially available alternatives, exclusive data sets, or government-issued concessions — these are moats. Climate tech in SEA is increasingly competitive, and investors are spending significantly more time on defensibility questions than they were two years ago.

EVC's Climate Tech Thesis

At Evolve Venture Capital, our climate tech focus in Southeast Asia is concentrated on three specific intersections:

- Dryland and arid-land energy systems (agrivoltaics, dryland solar with agricultural co-benefit)

- Blue economy infrastructure (aquaculture technology, blue carbon measurement and verification)

- Climate-adaptive agriculture (precision farming for climate-stressed conditions, water-efficient crop systems).

We’re not generalist impact investors looking for anything with an ESG label. We’re looking for specific commercial opportunities where the climate benefit is inseparable from the commercial model — where doing the right environmental thing and building a durable business are the same action, not trade-offs.

If you’re a founder building in any of these categories, or an institutional LP looking to understand our thesis in depth, explore our investment approach or reach out directly.

Frequently Asked Questions

Is climate tech in Southeast Asia investable at venture scale, or is it primarily a development finance category?

Increasingly both — and the two are intersecting in interesting ways. Development finance institutions (ADB, IFC, AIIB) are increasingly co-investing with venture funds in early-stage climate tech, which de-risks deals and provides patient capital alongside faster-return venture money.

What makes SEA specifically more interesting for climate tech than other emerging markets?

Three factors: geographic exposure (the region is among the most climate-vulnerable on earth, creating both risk and urgency), ASEAN net-zero commitments creating regulatory demand, and the convergence of marine, agricultural, and energy assets in a single interconnected geography. The blue economy opportunity in SEA is available nowhere else at this scale.

How do agrivoltaic projects handle land rights complexity in Southeast Asian markets?

The fundable companies have either partnered with established landowners under revenue-share arrangements or are working within government land allocation frameworks for renewable projects. Direct land acquisition is rarely the model — and investors generally prefer partnership structures to direct land exposure.

What’s the difference between blue carbon and traditional voluntary carbon credits?

Blue carbon credits are generated by protecting or restoring coastal ecosystems — mangroves, seagrasses, salt marshes — which sequester carbon at rates significantly higher per hectare than terrestrial forests. They tend to command premium pricing on voluntary markets because the co-benefits are measurable and credible.

How does EVC evaluate climate tech founders differently from conventional tech founders?

We weight regulatory navigation capability heavily — the ability to work within government procurement, land allocation, and environmental permitting processes is a core competency for climate tech founders in SEA. We’re also looking for founders who understand the carbon market deeply enough to structure revenue correctly.

The capital rotation into climate tech in Southeast Asia isn’t a story about investors becoming more idealistic. It’s a story about risk-adjusted returns shifting in favor of businesses that have government relationships, defensible IP, and multi-revenue-stream models in a market that is structurally, irreversibly moving toward net-zero compliance.

The window is real. It won’t stay uncrowded.

Explore EVC’s investment thesis or visit our portfolio to see where we’ve already committed capital in this space.