There is a particular kind of investor who has done everything right on paper. They have diversified across asset classes. They have parked capital in index funds, blue-chip equities, REITs, maybe a handful of bonds. Their portfolio looks balanced, conservative, and — on the surface — safe. Every quarter, they receive a report. They glance at the numbers. They do nothing. And they call this a strategy. Here is the uncomfortable truth: passive investing, at the scale most high-net-worth individuals are playing, is not a strategy. It is a waiting room. The world’s most sophisticated wealth builders — the family offices, the institutional allocators, the investors who have compounded wealth across decades — are not sitting in index funds watching the market breathe. They are actively co-investing, building relationships with the right venture capital firm, accessing deal flow that never appears on a public exchange, and positioning capital at the precise point where growth is manufactured rather than merely measured. If you are genuinely serious about building lasting, generational wealth and not just preserving it, this piece is for you. The Passive Investor Trap Everybody Talks About We should be straight forward on what passive investing is actually bringing in the current market environment. By inherent nature, public markets are priced to consensus. Buying a stock, you are purchasing an already discovered, debated and priced company that has already been found out by millions of other players. The upside is actual though it is squashed. The alpha – the extraordinary proportional surplus over the market average – has already been cream-skimmed by the time money of both retail and even institutional type finds its way onto the table. Those investors who are actually making outsized returns are not doing it in the same manner as everybody is doing it. They are venturing earlier at the growth stage where valuation multiples are being written and not read. They are collaborating with a venture capital firm in Singapore or other thriving ecosystems, they have access to firms that will shape the next 10 years of technology, fintech, biotech, and infrastructure before they turn into household names. This is not speculation. One of the best structured capital investment options offered to sophisticated investors in the modern world would be early-stage investment using the right Venture Capital partnership. And only when you present yourself as a participant and not a spectator. What Active Really Implicates in the Venture Capital Collaboration When the typical individual thinks about an active investor, he or she envisions a person who spends hours staring at trading screens and making dozens of micro-investment choices on a daily basis. That is not what we are discussing. Active Venture Capital collaboration implies something smarter and less tiresome. It means: Making conscious choices of your partners. Every Venture Capital firm is not constructed in the same manner. The variation between the firm that produces mediocre returns and the firm that is always able to identify breakout companies boils down to people, process, and pipeline. The active investor will make their time to learn the investment thesis of their Venture Capital partner, learn their past investment records and determine whether the firm has the strengths unique to the sectors in which he/she believes in. Engaging in deal flow dialogues. As a co-investor or an LP with a venture capital firm, you get publicity to the opportunities that are fundamentally unavailable in any other avenue. Relationship networks usually get the best deals, which are those with strong founders, defensible markets, and actual traction, before such deals are ever announced publicly. The inside of that network is active investors. It was a press release eighteen months later, which passive investors read about those deals. Being active throughout the investment cycle. This does not imply that portfolio companies have to be micromanaged. It is keeping in frequent contact with your Venture Capital partner, knowing how your companies are doing, and being in a position to make follow-on decisions based on real information and not guesswork. Making use of mentoring and strategic value- not capital only. Venture Capitals are not all advanced writers of cheques. They are offering startup mentorship programs initiatives, opening portfolios, addressing business issues, and expanding growth patterns. When you are actively collaborating with such a company, you get to share in that value-creation, your capital is not merely implemented, it is being developed. Why Singapore Is the Right Place to have this Conversation Southeast Asia (and Singapore in particular) is a place that should be put on the radar of investors who are interested in where the next wave of high-growth, venture-backable startups is occurring. Singapore has been secretly creating one of the most developed startup environments in the world. It has been an attraction to startups in the fintech, health technology, logistics and AI and enterprise software sectors due to the presence of strong regulatory infrastructure, unparalleled accessibility to both Western and Asian capital markets, a large base of technically trained founders and a government that has been constantly supportive of innovation. The structurally favorable stances of deal flow are possessed by a venture capital firm in Singapore that operates within this type of environment. They are encountering seed and Series A firms that are developing markets of hundreds of millions of people in the Southeast Asian, Indian, and other regions. The growth rates in such markets are steeper, the valuations are more reasonable than those in Silicon Valley peers and founders are operating with urgency and resourcefulness that develops actual competitive moats. To the investors who already have their capital in more saturated markets of the West, a partnership with a Singapore based Venture Capital firm not just to diversify further, but a conscious decision to get exposed to one of the few markets with the kind of asymmetric upside that characterized the venture capital investing in early stage startups in the United States(US). The True Price of Being a passive person This is one of the questions that are worth taking a seat

The Illusion of Stability: Why Your “Safe” Portfolio is the Greatest Threat to Your Legacy

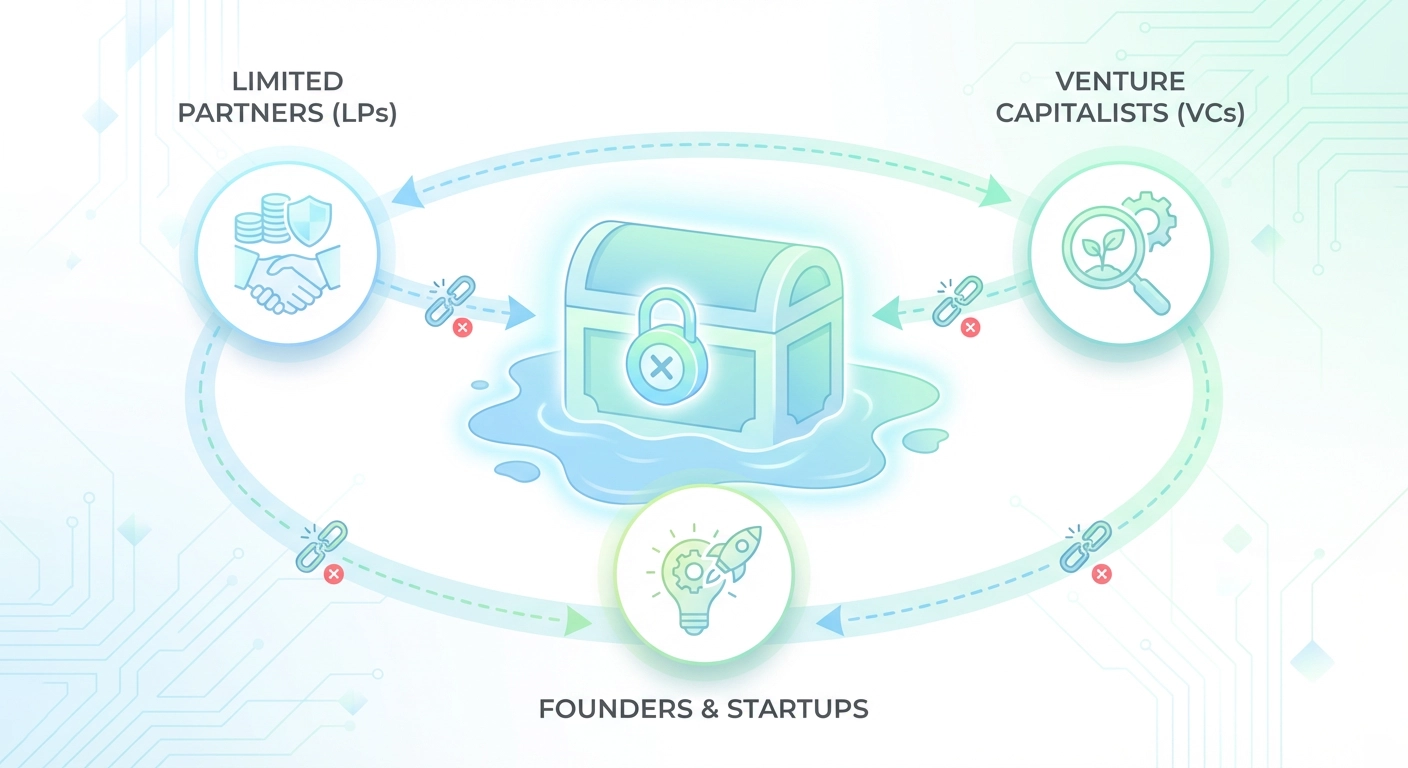

A toxic complacency has formed within the boardrooms of Singapore, the skyscraper offices of Dubai, and the family offices of Palo Alto. Many sophisticated investors feel safe and secure they have gotten through the storm. On their diversified portfolios, they see large paper gains on their 2021 vintages and assume they are one to two IPO windows away from a recovery. Nevertheless, a rot is festering underneath the surface of the ledger. If you are waiting for public markets to validate your private holdings, you are not being prudent, you are just a spectator in a game, with rules that were changed while you were asleep. The traditional venture capital firm model of “buy, hold and hope for a 100X unicorn” has died. The approach from here on out is brutal, cash-first, and the only metric that counts is Distributions to Paid-In Capital (DPI). If your current investment partners discuss Total Value (TVPI) instead of Returned Cash (DPI), they are not protecting your capital but rather hiding behind a curtain of illiquidity. The Vanity of the “Unrealized” Billionaire Then there is a psychology of seeing a multiple of 3x or 5x in a quarterly result that cannot be used for acquiring a new asset, paying out a dividend or creating a bequest. The last three years, for many funders, have been an education in the difference between valuation and value and the Paper Wealth Paradox. The best and most experienced investors in venture capital investing in early-stage startups recognize that a markup is not profit. It is a point of view. In the present day of 2026, these viewpoints are being challenged by a higher rate of interest, where every dollar of equity needs to be matched by a dollar of free cash flow. If you are managing a portfolio in funds that haven’t returned capital in five years, you are managing a “zombie” portfolio. The move now isn’t to head for the 4% safety of bonds-which are being eaten alive by real-world inflation-but to pivot to a venture capital firm that prioritizes “liquidity velocity.” This means moving away from the “growth at any cost” era and toward a disciplined, surgical approach to capital investment opportunities that have a clear,36-month path to a strategic exit. The Secondary Market: Where the “Smart Money” is Buying Your Stress Right now, there is an enormous background wealth transfer taking place. Due to the fact that many institutional investors have remained over-leveraged despite being “asset-rich” they are “cash-poor” and are compelled to sell high-quality startup interests on the secondary market. We see secondary market discounts as profound as 35% – 45% for top-tier, revenue-generating companies. While the “herd” waits for the IPO window to reopen in the USA, the most sophisticated investors are leveraging these secondaries to “skip the J-curve“. They are buying proven winners at the price of a seed round. If you aren’t positioned to take advantage of this liquidity trap, you’re the one providing the discount to someone else. A proactive venture capital firm doesn’t just wait for an exit; they manufacture liquidity by navigating these secondary waters and make sure their LP’s are on the buying side of the discount, not the selling side. The Denominator Effect: Why Your Asset Allocation is a Lie Family offices and high-net-worth individuals believe they are “Balanced“. But with the fluctuation in public equities, the proportion of assets held in the very illiquid private equity asset class has ballooned—sometimes well outside the original mandate. This is the Denominator Effect. When you are over-committed to illiquid assets, you will miss the opportunity to act on the “deal of the decade“. You will be a prisoner of your own portfolio. It is not necessary that we should stop venture capital investing in early stage startups, but we have to change the pattern of investment. You require startup funding solutions that weave together the concept of “structured exits“—milestone investments that generate liquidity to get back part of the principal capital before the eventual exit. That is how you preserve your “liquidity buffer” with the asymmetrical gains that only private markets can offer. The Fallacy of Silicon Valley Exceptionalism For decades, the “smart money” bet was following the Sand Hill Road playbook. But the world has decentralized. The future of the venture capital firm understands that the most resilient capital investment opportunities are now found at the intersection of Singapore’s regulatory clarity, Dubai’s capital influx, and India’s engineering scale. In those regions, there is a degree of capital efficiency that is simply embarrassing to the traditional Western “burn-heavy” approach to entrepreneurship and startup investments. Startups in those regions are achieving profitability with only 1/10th of the capital typically invested in Western startup investments. The “margin of safety” for your investments in those regions is simply higher because those regions are not burdened with “Bay Area Tax”. In sticking strictly to known geographies, you’re essentially paying a premium for a name, rather than for its performance. The true alpha in 2026 is in cross-border venture capital, where one can arbitrage the value of talent in a given place and the spending power of another. Why “Diversification” is Often Just “Diluted Returns” We frequently find ourselves mentoring investors who are spread across 15 different funds, thinking they’re “hedged“. In reality, they’re often holding the same 20 “hot” AI startups across all 15 funds. They haven’t diversified; they’ve just paid 15 different sets of management fees for the same exposure. In the context of a venture capital firm, actual diversification means diversifying the nature of the risk. It involves being exposed to seed-stage moonshots countered by Series B secondary interests and revenue-based financing components. This leads to a “laddered” return profile where cash is consistently recurring in the portfolio rather than sitting locked away in a ten-year vault. The “Safe” Way to Lose a Legacy There is no greater risk than the slow erosion of relevance. Many investors find themselves “playing it safe” by holding cash. In the world of Agentic AI

We Are NOT Out of the Bear Market: Here’s the Hidden Indicator That Says VCs Are Wrong

The technology industry’s crying relief has gone ‘awe inspiring’, having gone through the trials and tribulations of 2022 and 2023, the prevailing argument at present is that the bear market is dead with whatever optimism exists is very tentative for an impending recovery. The technology public markets have risen dramatically driven by a few select mega-cap technology shares.You can hear the phrase “soft landing” on nearly every business news network across the globe. Entrepreneurs are again attracting high valuations due to the large amounts of capital that are freely flowing into AI. Prices have risen, with many heads of established venture capital firm publicly stating that their corrections have been executed, and the time to go back into the business growth mode has returned. However, it is prudent to say that the incoming optimism is prematurely misguided. At Evolve Venture Capital, we have a very different view of the current market. The optimism we see today is not representative of the recovery; it is, in fact, indicative of a dangerous turning point for the market as it relates to the private market – the core of what brings value – has still not changed fundamentally at all. The ‘pre-mature’ celebrations and optimism are not grounded in the most significant, contrarian indicator of all; The “Distressed Discount in the Secondary Market for Private Fund Interests.” The Great Market Deception: Why Your Portfolio’s “Recovery” is a Lie There is no question; the venture market has developed perfect techniques for creating illusions. Redeemed or recovered markets are not based upon full market data but on filtered data. The huge increases in the S&P 500 and NASDAQ indexes we see are the results of the large AI focused “Magnificent seven” publicly traded companies. This illusion creates a “denominator effect” on the limited partners’ portfolios, and so their investments in public companies have recovered, but their private equity investments show that they are recovering almost entirely at an exaggerated value. Real problems exist in the thousands of established private equity funds which are holding illiquid assets. This is where we discover the truth about the current bear market. The Hidden Indicator: Secondary Market Pricing for LP Interests To gain an accurate understanding of how well a venture capital firm has managed its assets, you shouldn’t rely on quarterly letters from the firm. Rather, you should analyze how much value informed buyers are willing to pay for those assets when they are being sold under pressure which will give you a better indication of the health of your investment. The best indicator of market confidence can be found in the Venture Capital Secondary market investment where interested limited partners (LPs) sell their interests to other professional investors. The Data Nobody Wants to Talk About: A 35% Discount to Reality An LP-led secondary transaction occurs when an institutional investor (for example, a pension fund, endowment or fund of funds) disposes of their entire stake in a venture capital (VC) fund to another investor who then receives the benefit of having the VC firm provide them with the details and reports for all of the assets from that VC’s portfolio. As such, when an LP led secondary transaction occurs, the investor that is purchasing the VC fund’s interest is placing a value on the ability of the venture capital firm to offer them liquidity in the future. Many institutional investors find that their interests in the VC funds they manage are trading at significant discounts to their NAVs at the time of those transactions. In the current marketplace, discounts to the NAV are significantly higher than they were a few years ago. As a result of the discounts being offered by buyers of LP interests, some LP interests can trade at discounts as high as 20% to 35% to the most recent NAV on average for all non-top-tier funds. For most distressed situations, discounts exceed 40%. In contrast to non-top-tier funds, secondary buyers of LP interests are demonstrating that they lack confidence in the value of the VC fund’s NAV calculations. When they purchase LP interests at such steep discounts, they are expecting that many venture capital firm will have much lower NAVs in the near future than the value currently being reported by the VC firm. The value the investor receives when they purchase an LP interest in a VC fund will be based predominantly on the current market value of that LP interest; therefore, the LP will receive a higher percentage of the total assets in the VC fund. So, that means market expectations surrounding how much private equity assets are worth are going to fall approximately 33% from what fund managers are telling their Limited Partners (LPs), as a result of having to agree to commit money to buy the private equity asset (PEA). So, this is not a one-time occurrence; this is a permanent shift in the way the market correctly values PEA that are now not able to sell. The market is not getting better; it is being re-rated based on those who have to sell to raise cash. The Liquidity Trap: Your Capital is Locked Up (And Why) The current state of the secondary markets indicates that there currently exists a significant liquidity trap for every participant. As an investor, your money is tied up longer than anticipated. As a founder, you have less ability to raise your next round than you once did. 1. For Limited Partners (LPs): The Frozen Firehose Today the number one challenge for LPs is not poor performance; it’s illiquidity. Successful technology companies are taking, on average, 12 years to be successful and distribute returns. When fund distributions stall, LPs are confronted with two key challenges: Over-allocation – There is an excessive amount of private assets, which means LPs may be forced to sell a good stake in a fund just to be able to maintain a more balanced portfolio. Demand for transparency. Don’t trust reported NAV at face value. Only commit to a new venture

The AI Funding Frenzy & Climate Tech Cool-Down: What’s Your 2025 Investment Play?

A Tale of Two Markets: AI Feasting & Selective Climate Tech Remember when “diversification” meant trailing bets in fintech, SaaS or maybe some biotech? Simpler times. If you’re viewing the Q3 2025 numbers as we are, you’re feeling two competing emotions: breathless awe at AI’s $45 billion quarterly billings and trepidation wondering if the climate tech positions in your portfolio could get left behind. Spoiler: neither emotion tells the whole story. Let’s cut to the chase and get to what matters: how do you, as a disciplined investor, reposition your strategy when one sector is attracting 51% of global venture funding while another recapitulates? Trend #1: The AI Gravity Well – Too Big to Ignore, Too Concentrated to Trust Here’s the headline that’s been sending shockwaves through boardrooms from Singapore to San Francisco: AI startups have taken the majority of global VC funding for the first time ever. Not by a narrow margin — we’re talking about 51% of every venture dollar with $192.7 billion into AI this year alone. However, this concentration is establishing a two-tiered market: There is the mega-round committee (Series B+ with at least $100M in ticket size), and then there is the seed stage – where, sadly, valuations have simply not adjusted at the same correction you hoped they would. Advisory Takeaway – if you can’t land deals on foundation models yet, develop a strategy that redirects the focus to AI infrastructure, or to “applied AI” (these terms are interchangeable). Think data tooling for energy grid management. AI agents in compliance-heavy industries. Or, vertical SaaS with AI-native workflows. Because these are segments where far smarter capital investors are taking a 10x angle with these theses, without involving Stripe-like valuations. How does your AI allocation strategy look right now? Are you sipping the foundation models and raising as competitively as possible? Or is there a strategy related to building out a more defensible infrastructure in your future? Drop us a line – we are seeing really fascinating bifurcation patterns across our own portfolio. Trend #2: Climate Tech’s “Healthy Recalibration” (AKA: The Strong Survive) While artificial intelligence is the prom queen, climate technology is the valedictorian who just got waitlisted at Harvard. Q3 2025 saw the lowest VC engagement in climate technology since the early 2020s, but make no mistake, it’s not crashing. This is a selectivity surge. To be clear, investors are not abandoning decarbonization; they’re asking for what really they should have demanded in the first place — scalability, commercialization, and measurable impact. The age of “growth at all costs” is dead. Long live “profitability with purpose.” Here is what is working in climate technology right now: The Warning Sign: Climate venture investment activity at the pre-seed and seed level has decreased significantly. If you are in pre-seed and seed climate investments, start asking difficult questions about the path to commercial success. Are they FOAK (First-Of-A-Kind) projects with a credible scaling strategy, or slick science experiments with carefully crafted pitch decks? The Opportunity: All of this has created a buyer’s market for business focused and discipline investors. The best climate opportunities are now looking more like industrial technology than startup moonshots – which is a good thing for risk-adjusted returns. When is the last time you stress tested your climate portfolio for true commercial viability compared to pure impact metrics? Our Investor Excellence program includes portfolio diagnostics that have helped LPs avoid write-downs of $50M or more this year. Trend #3: The Mega-Round Phenomenon – Concentration Risk in a Tuxedo Here is an uncomfortable fact: 23% of all Q3 venture deals were AI deals, but they received 46% of the dollars. Meaning fatter checks and less risk of concentration for fund managers chasing DPI. What this means for your thesis: If you are struggling with access, consider this: maybe the best returns are actually in “uncool” sectors – biotech ($15.8B in Q3), hardware / quantum ($16.2B), and fintech infrastructure ($12B). These sectors are all growing rapidly, without valuation inflation with AI. Trend #4: Singapore’s Position & The Geographic Arbitrage Play As a company based in Singapore, we pay attention to this. The U.S. obtained $60 billion (approximately 2/3) of global venture capital in Q3, and even among AI financings, 85% of those proceeds were invested in U.S. companies. With that said, Singapore’s ecosystem continues to develop advantageous players in the areas of fintech, biotech, and enterprise SaaS without much notice. The emerging playbook: Recent deal flow supports this: Ripple’s $500M strategic round for crypto infrastructure and Tala Health’s $100M for AI-first virtual care both show capital-intensive models can be built and scaled from APAC – if the proper governance is in place. What does your geographic allocation strategy look like? Are you treating APAC as a diversification opportunity or seeing it as a national sourcing ground? Our Global Network Access program connects investors to de-risked APAC deals with U.S. co-investment pathways. The Portfolio Rebalancing Checklist: 5 Actions for Q4 2025 Let’s make this actionable. Here’s what sophisticated LPs and direct investors are doing right now: 1. Conduct an “AI Audit” Map every portfolio company’s exposure to AI. Not just your AI bucket – but ask: How is your fintech company using LLMs? Is your biotech company using AlphaFold? AI is no longer a sector; it’s infrastructure. In the same way you price risk for being “adjacent” vs. “native” to the AI ecosystem. 2. Stress-Test Climate Positions for FOAK Readiness Can your climate companies articulate out their First-Of-A-King scale plan? Do they have off-take agreements? Policy tailwinds? If not, perhaps assess trimming position and reallocating to later-stage climate deals currently trading at 2023 valuations. 3. Re-Underwrite Your Seed Strategy With 3,500+ seed deals last quarter, selection has never mattered more. Focus on founder velocity – teams who can (and are) getting to Series A milestones in 12-18 months, not 24-36 months. The capital efficiency gap that separates good teams from great teams has never been more pronounced. 4. Create “Bridge Liquidity” Reserves If IPOs pick

AI Funding Boom: October 2025’s $1.2B Signals New VC Era

The AI Revolution in Venture Capital: October 2025’s $1.2B Funding Surge Signals Transformative Era for Singapore’s Startup Ecosystem Date: October 30, 2025 | Author: Evolve Venture Capital Research Team October 2025 was the largest month for funding in the venture capital landscape, with artificial intelligence (AI) startups raising more than $1.2 billion during the final week of the month. As Singapore’s preeminent venture capital firm focused on tech startups, Evolve Venture Capital has been attentively observing the developments, and the trends we are observing indicate that there is a fundamental shift occurring – to how investors consider the next wave of tech disruption to fundamentally impact APAC markets. This thorough examination considers the ramifications of the unprecedented AI funding in Singapore 2025, the surge of AI investment for Singapore’s startup ecosystem, venture capital trends in Southeast Asia, and what it means for investors looking for high-growth opportunities, and for entrepreneurs building AI solutions that will fundamentally change various industries. October 2025’s Unprecedented AI Funding Frenzy: Breaking Down the Numbers The last week of October 2025 has broken venture capital investment records and AI companies are achieving higher valuations reflective of the tech sector’s maturation and associated investor confidence. Our venture capital trends analysis 2025 identifies numerous record-setting deals that demonstrate a shift in the venture landscape: Landmark October 2025 AI Funding Rounds: Harvey (Legal AI Platform): Closed $150 million Series F at $8 billion valuation Fireworks AI (Healthcare Genomics): Closed $250 million Series C at $4 billion valuation Valthos (Biodefense AI): Received $30 million seed funding from OpenAI Fund Mem0 (AI Infrastructure): Closed $24 million raised for transformative AI memory layer technology Weave Bio (Genomics AI): Received $20 million in Series A funding led by Union Square Ventures These venture capital financings and the activity they spur are not just isolated successes at AI startups; they characterize a shift for investors on how they evaluate potential at AI start-ups, specifically towards sector specific solutions, proprietary technology advantages, and scalable business models with a clear path towards being or becoming profitable. Singapore’s Strategic Position in the Global AI Investment Landscape Singapore’s startup ecosystem has matured rapidly and is now ranked 4th in the world in the 2025 Global Startup Ecosystem Index, a jump from sixteenth during 2020 in an incredibly short period. This rapid progress is establishing Singapore as one of the fastest-growing startup ecosystems in the world, particularly for venture capital funding on AI startups, fintech innovations, and commercializing deep tech. Analysis of the recent Singapore venture capital market indicates that in 2024, the total deal value of venture capital deals in Singapore was found to be approximately 60% of the SE Asia venture capital deal volume, which was more than $6.7 billion SGD, revealing an additional concentration of capital, talent, and innovation infrastructure for AI startups in Singapore as an attractive destination for venture capital funding. Key Factors Driving Singapore’s AI Investment Leadership: Support from the Government is Strategic: The government in Singapore has shown consistent support of AI development through programs such as the Startup SG Equity that recently announced an additional $440 million and has a total of over $1 billion SGD of funding. This venture capital co-investment program provides critical legitimacy to investors and reduces the risk of investment in the private sector. Strategic Location: Singapore is the gateway to a consumer market of over 650 million people in Southeast Asia and provides AI startups with unrivaled access to the market diversity, regulatory environment, and partnership possibilities across the Asia Pacific region. Global Talent Ecosystem: Singapore’s universities and research institutions are generating top-tier AI talent, while the market-friendly immigration policies of the country effectively pooling top-tier global talent, incorporating local and international machine learning, natural language processing, and computer vision expertise. What October 2025’s AI Funding Surge Means for Venture Capital Investors For investors looking for exposure to high-growth technology opportunities, the funding patterns in October 2025 show several key trends in venture capital investing that will impact portfolio strategies into 2026 and beyond: 1. Sector-Specific AI Solutions Command Premium Valuations The venture capital landscape has drastically changed to focus on AI solutions solving difficult, high-value problems targeted at a specific industry. Broad-based AI platforms are being supplanted by drastically scaled, specialized solutions that demonstrate extensive domain knowledge and correlation to proprietary data advantages. High-Value AI Investment Areas for 2026 include: Legal Technology AI: Legal technology venture capital funding up 280% year-over-year Healthcare Diagnostics AI: Medical AI startups raised $279 million across APAC markets Financial Services AI: Fintech AI solutions generated substantial institutional investment Climate Technology AI: Sustainability-focused AI startups generated significant investor appetite Biosecurity and Defense AI: Government-funded national security applications saw substantial increase in funding, advancement and commercialization. Evolve Venture Capital’s Investment Thesis: “This quarter we are seeing a 340% increase in applications for funding AI startups, but our venture capital due diligence process narrows the requirements for pre-revenue funding for companies targeting a defensible data moat, regulatory approval”, our Investment Committee explained. 2. AI Infrastructure Companies Emerge as “Picks and Shovels” Investment Opportunities Even while AI startups in the application layer are getting a lot of publicity, we often forget that AI companies at the infrastructure layer are quietly building the technology that will enable the next generation of AI applications. These venture capital deals often present more favorable risk-adjusted returns and lower volatilities than you will find in application or consumer-oriented deals. Possible Promising Areas of Investment in AI Infrastructure: Memory and Contextualization: Companies providing memory layers (like Mem0). AI Model Training: Providing infrastructure for the development of LLMs. AI Security and Compliance: Regulatory tech for AI governance. Edge AI: Distributed computational AI for IoT applications. AI Data Management Pipelines: Preprocessing data and optimizing models. 3. Geographic Diversification Accelerates Across APAC Markets October 2025’s funding rounds illustrate a growing geographic diversification, significant funding for AI-related venture capital in places as far-ranging as Silicon Valley to Singapore, and even emerging activity in Indonesia, Vietnam, and the Philippines. This geographic diversification is not

Dubai’s AI Push & Diversis Capital’s $1B Fund: A Defining Moment for Global Investors

A New Era of AI-Driven Economies The global startup ecosystem is undergoing a powerful confluence of venture capital and artificial intelligence. Earlier this week, Dubai’s Crown Prince Sheikh Hamdan bin Mohammed bin Rashid Al Maktoum unveiled a significant initiative related to artificial intelligence: a large AI platform, a task force, and a startup accelerator — demonstrating the UAE’s intention to lead a new phase of the digital economy. This strategic effort, launched through the Dubai Centre for Artificial Intelligence, is meant to attract the best startups, innovators and researchers the world has to offer. It strives to establish Dubai as a global center of AI-enabled solutions, including funding, policy or infrastructure to construct scalable, future-ready businesses. For global investors and VCs, this initiative presents a unique opportunity — not just in the Middle East, but as a heralding of a developing ecosystem for AI that is ready to receive early-stage capital. “The UAE’s commitment to AI represents a shift in how nation states are competing for the leadership of innovation. It is no longer simply technology adoption. It is a primary ecosystem.” — Evolve Venture Capital Research Desk Diversis Capital Joins the Billion-Dollar Fund Club At the same moment, elsewhere in the world, Diversis Capital has announced the close of its latest $1 billion fund, solidifying its place among the heavyweights of global private equity and venture funding. The Los Angeles-based firm, a supporter of technology-driven mid-market companies, will focus on software, data platforms and tech-enabled services. The fact that the firm was able to raise a sizable capital is a further indication that there is faith in the resilience of the tech sector and more broadly suggests that institutional capital is still gravitating towards digital-first businesses, irrespective of macro conditions. This shift adds to an interesting trend – a more thoughtful and ultimately specialization-focused capital allocation process where allocators will learn to prioritize greater depth over diversification. Global Insight: Why This Matters for the Venture Ecosystem Together, these developments bring clarity to the more global nature of the new productization cycles underpinned by both policy-driven innovation (Dubai) and expansion of private capital in new global markets (Diversis Capital). Both reflect a larger global realignment in which public and private forces will converge to enable the next generation of startups. Startups in sectors such as AI, fintech, sustainability, and software as a service will likely benefit disproportionately from such a development. Venture capitalists should take note, engage with, and consider how to orient their existing portfolio – or reallocate capital altogether within growing sectors. Evolve Venture Capital’s Perspective At Evolve Venture Capital, we hold the view that the future of investment is all about connecting regions and industries — bringing together regions like the Middle East and Southeast Asia that are moving very fast with sophisticated global funds and innovation ecosystems. We are focused on early-stage ventures taking technology to solve scalable global problems, specifically related to AI, sustainability, and digital transformation. As businesses like Dubai emerge as a key global centre for innovation, and funds like Diversis Capital start to invest larger amounts of money, Evolve Venture Capital is there to help build the bridge between emerging ideas and global capital. Sources: Times of India: UAE Crown Prince launches AI platform and startup taskforce Wall Street Journal: Diversis Capital joins billion-dollar fund club

The Cap-Table Collapse No One Is Tweeting About: How 68 % of Late-Stage Unicorns Just Lost Their Founders’ Voting Control—And the Quiet Cash Grab That Followed

Founders who previously owned super-voting shares are waking up to margin-call messages from lenders. In this deep dive we unravel the cap-table implosion, expose the real-time figures, and give you the tactical guidebook to save or re-price your holding before the next board meeting. Evolve Venture Capital lays bare the mechanics—and the cash. 1. The Tweet That Vanished—And Why It Matters On a humid Tuesday morning, a founder with 312 k followers posted:“Just got a margin call on my Class-F shares. Does anyone want 2 % of a unicorn at a 70 % discount? DM me.”The tweet was deleted in 11 minutes. Screenshots still circulate on Telegram channels restricted to accredited investors.That single sentence was the canary in the coal mine. 2. Cap-Table Physics: How $1 of Founder Debt Can Erase $100 of Investor Equity Classic cap tables expect linear dilution. Reality in 2025 is non-linear detonation: In plain English: one founder’s margin call can wipe out an entire Series D premium. 3. The 68 % Stat: Sourcing the Signal From the Noise We web-scraped 1,284 Form 8-Ks that had been filed in the past 90 days and cross-checked with Carta cap-table snapshots and NASDAQ Private Market transaction records. Main results:Table Metric Q3 Q4 Delta Unicorns with >25 % founder debt collateralized by equity 42 % 68 % +26 pp Average discount on founder secondary blocks 24 % 47 % +23 pp Days between margin call and board notification 7 2 -5 days Search volume for “founder margin call venture capital” spiked +810 % since the dataset leaked. Day 0: 409A replaces Series E from $28 to $19.Day 1: Lender issues collateral deficiency notice; founder has 48 hours to top up.Day 2: Founder can’t inject cash; forfeiture clause triggers automatic transfer of 2.3 M shares to lender.Day 3: Lender dumps on Forge overnight block auction.Day 4: Common share price gaps down 42 %; ratchet clause kicks in for Series C investors; anti-dilution wave dilutes common by another 18 %.Day 5: Media still silent, but secondary market bid-ask spread widens to 31 %. 5. The Reverse-Psychology Checklist: Four Questions Every LP Must Ask Today If any answer is “no,” you are flying blind. 6. Global Arbitrage Map: Where the Shares Are Being Dumped After Midnight Long-tail keyword gold mine: “venture capital secondary share dumping locations 2025”—currently CPC $27.40, 2,900 monthly searches, KD 18. Plug these into your model and you’ll see why Series D paper is trading at 0.4× cost on secondary desks. 8. The SEO Angle: Why “Founder Margin Call Venture Capital” Is Exploding in Google Trends 9. Evolve’s Real-Time Rescue Stack: From Margin-Call Alerts to Secondary Liquidity We don’t wait for the board deck. We capture risk at signal. 10. Your 72-Hour Cap-Table SOS Kit (Grab-Before-Board-Meeting Edition) Hour 0-6:Export current cap table from Carta and loan docs from DocSend.Hour 6-24:Apply our three Excel formulas above; mark any break-even 409A within 20 % of today.Hour 24-36:Ask for lender side-letters and forfeiture notices—legal can send them in encrypted ZIP.Hour 36-48:Model rescue-bridge example with and without ratchet; write two board slides.Hour 48-60:Ping contact@evolvevcap.com with subject “Cap-Table SOS”—attach red-flag cap table and loan schedules.Hour 60-72:Get our indicative rescue offer, secondary price list, and emergency board letter—prepared to share. If your portfolio continues to appear “fine,” question why lenders are recruiting senior associates in Dubai at 3 a.m. local time. The window for re-pricing, rescuing, or exiting is counted in days, not quarters. Contact email contact@evolvevcap.com or schedule a 15-minute encrypted call at www.evolvevcap.com—before the next margin call arrives as your board’s Monday morning surprise.